Personal Finance

How High Interest Rates Affect Household Budgets

Understand rising borrowing costs and protect your monthly finances.

Many households today feel financial pressure even though inflation has slowed. Monthly bills remain high, savings grow slowly, and large purchases feel harder to afford. The common question is simple: Why does money still feel tight?

This guide explains how high interest rates affect household budgets, how they change spending decisions, and what practical steps households can take to manage financial risk. You will learn which expenses are most sensitive to interest rates, who is affected first, and what signals to watch when planning major financial decisions.

As of 03/18/2026 (ET), the Federal Reserve maintained the federal funds target range at 3.50% to 3.75%, keeping borrowing costs elevated. On 04/16/2026 (ET), the average 30-year fixed mortgage rate was 6.30%, limiting housing affordability. Meanwhile, total U.S. household debt reached $18.8 trillion at the end of Q4 2025, reflecting continued growth in credit card and auto loan balances.

The key idea is straightforward: when interest rates stay high, debt becomes more expensive. Over time, higher payments reduce financial flexibility and reshape everyday spending.

---

Why Interest Rates Still Matter After Inflation Slows

Inflation may fall, but interest rates can remain high for longer. That difference explains why many households still feel pressure in 2026.

Interest rates directly affect borrowing costs. When rates remain elevated, lenders charge more for credit cards, auto loans, and mortgages. Even households that stop borrowing can feel the impact because existing debt becomes more expensive to maintain.

This situation matters because many types of consumer debt adjust quickly when rates change. Credit card balances, variable-rate loans, and new financing respond faster than wages or savings.

In practical terms, the pressure has shifted from rising prices to rising payments.

---

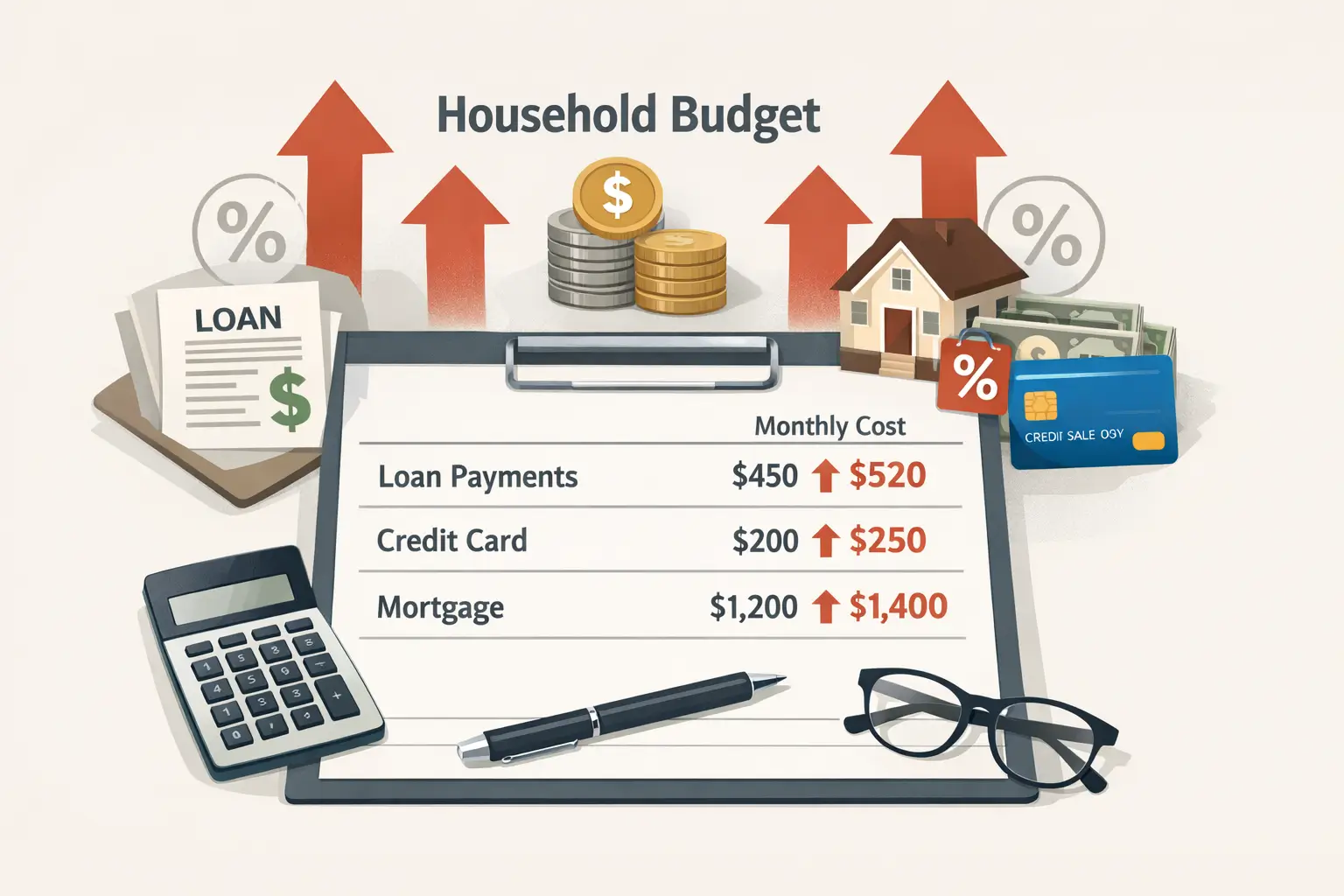

How High Interest Rates Increase Monthly Expenses

Higher interest rates influence budgets through one primary channel: financing costs. When rates rise, required payments increase, leaving less money available for other needs.

Three expense categories typically feel the impact first.

Credit Card Payments

Credit cards often carry the highest interest rates among common household debts. When rates increase, minimum payments rise and balances take longer to pay off.

This reduces flexibility in monthly budgets and increases financial stress over time.

This trend becomes more pronounced when interest rates remain elevated for long periods. See also: Why Credit Card Debt Keeps Growing in 2026.

Auto Loan Costs

Vehicle financing has become more expensive in recent years. Higher rates combined with elevated vehicle prices create larger monthly payments.

Transportation costs can quickly become one of the largest household expenses.

Mortgage Affordability

Mortgage rates above 6% reduce purchasing power for buyers. Households qualify for smaller loans and may delay moving or upgrading homes.

This can limit financial mobility and slow housing activity.

---

Who Feels the Impact First

High interest rates affect households differently. Some groups experience financial pressure earlier and more intensely.

Recognizing these patterns helps households plan ahead and helps investors identify early economic signals.

The most affected groups typically include:

Lower-income households

They often rely more on credit and have fewer savings to absorb higher payments.

Younger households

Many entered the housing or auto markets recently and locked in higher borrowing costs.

Borrowers with variable or revolving debt

Their payments adjust quickly when interest rates rise.

These groups often show signs of financial stress before broader economic changes appear.

---

Practical Ways to Adjust Spending in a High-Rate Environment

Households rarely make sudden financial changes. Instead, they gradually adjust spending priorities as borrowing costs rise.

Common adjustments include:

- Delaying home purchases

- Postponing vehicle upgrades

- Reducing discretionary spending

- Slowing savings growth

- Paying down debt more cautiously

These changes help stabilize budgets. However, they can also reduce overall consumer spending, which plays a major role in economic growth.

---

Risks to Watch When Interest Rates Stay High

High interest rates do not automatically create financial problems. But they increase vulnerability, especially when debt levels are rising.

Four indicators provide early signals of financial stress.

1. Federal Reserve Policy Decisions

Changes in interest rates directly affect borrowing costs. Lower rates typically reduce monthly payments over time.

Understanding when rate cuts may happen is critical for planning borrowing and refinancing decisions. See also: Rate Cuts May Slip Again — Watch These 3 Signals

2. Inflation Trends

Stable inflation allows policymakers to consider reducing interest rates. Rising inflation can delay relief.

3. Refinancing Activity

An increase in refinancing usually signals improving financial flexibility. Low refinancing activity suggests households remain locked into higher payments.

4. Consumer Credit Stress

Rising delinquency rates in credit cards or auto loans often indicate growing financial strain. These trends can affect lenders, retailers, and employment conditions.

Monitoring these indicators helps households prepare for financial changes before they become urgent.

---

Smart Financial Strategies During Periods of High Interest Rates

Households cannot control interest rates, but they can control how they manage debt and spending.

Practical strategies include:

Paying down high-interest debt first

Reducing credit card balances lowers interest costs quickly.

Maintaining an emergency fund

Savings provide protection against unexpected expenses or payment increases.

Reviewing major purchases carefully

Delaying large expenses can improve financial stability during high-rate periods.

Tracking interest rate trends

Understanding rate direction helps households plan refinancing or borrowing decisions.

These steps improve financial resilience without requiring major lifestyle changes.

---

Conclusion: High Interest Rates Change Budgets Gradually

High interest rates reshape household budgets over time rather than all at once. The effects appear first in monthly payments, then in spending decisions, and eventually in broader economic activity.

The practical takeaway is clear: managing debt becomes more important when borrowing costs remain elevated. Monitoring interest rates, refinancing opportunities, and credit conditions helps households stay prepared.

Looking ahead, the most important factor is how long interest rates remain high. That timeline will determine whether household finances stabilize, tighten further, or begin to recover.

---

FAQ

Why do household budgets feel tight even when inflation is lower?

Because borrowing costs remain elevated. Higher interest rates increase payments on credit cards, auto loans, and mortgages.

Which expenses are most affected by high interest rates?

Credit card payments, auto loans, and housing costs typically rise first because they rely heavily on borrowing.

Who is most vulnerable to high interest rates?

Lower-income households, younger borrowers, and people with variable or revolving debt are usually affected earliest.

When will interest rates start to fall?

Interest rates typically decline after inflation stabilizes and central banks determine that economic conditions allow for lower borrowing costs.

---

Sources and Further Reading

- Federal Reserve — FOMC Statement — 03/18/2026

- Federal Reserve Bank of New York — Household Debt and Credit Report — 02/2026

- Bureau of Labor Statistics — Consumer Price Index Summary — 03/2026

---