Personal Finance

How Rising Living Costs Change Household Budgets

Learn how households adjust spending and savings in a higher-cost economy

Many households are asking a simple question: Why does everyday life still feel expensive, even when inflation is slowing? This guide explains how rising living costs change household budgets, which expenses create the most pressure, and how families can adapt their financial plans.

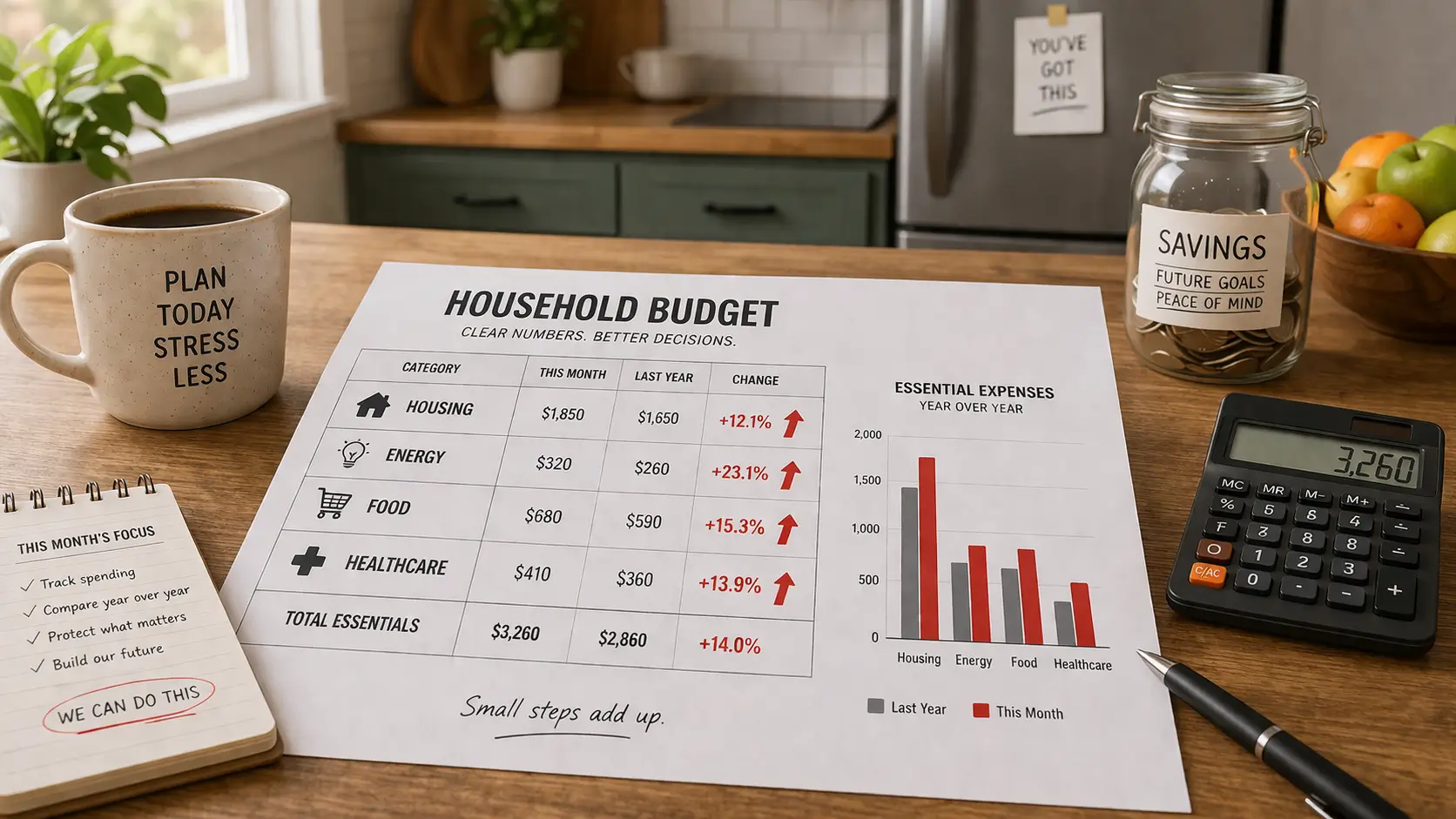

The issue is not just short-term inflation. It is the lasting impact of higher prices on essential expenses. The Consumer Price Index rose 3.3% year over year in March 2026, while energy prices increased 12.5%, and gasoline surged 18.9%, representing one of the largest monthly increases in energy costs in decades. These shifts have changed how households spend, save, and manage risk.

Understanding these changes helps households make better financial decisions and helps investors and professionals interpret broader economic trends.

---

Why Household Budgets Feel Tighter Today

The Shift From Temporary Inflation to Higher Baseline Costs

Inflation surged in 2021 and 2022, but the long-term effect is not just higher prices — it is a permanently higher cost base.

Even when inflation slows, prices rarely fall back to previous levels. Instead, households adjust to a new normal.

Key indicators show this shift:

- Consumer Price Index: +3.3% year over year (March 2026)

- Energy prices: +12.5% year over year (March 2026)

- Gasoline prices: +18.9% monthly increase (March 2026)

- Housing costs: One of the largest ongoing drivers of household expenses

- Food prices: Remaining above long-term averages

This environment requires long-term budgeting strategies rather than short-term reactions.

Why This Matters for Financial Stability

When essential costs rise, households must make trade-offs. Spending shifts toward necessities and away from discretionary purchases.

Over time, these adjustments influence:

- Savings behavior

- Debt levels

- Investment decisions

- Economic growth

Because consumer spending represents roughly two-thirds of U.S. economic activity, changes in household budgets affect the entire economy.

---

The Expenses That Put the Most Pressure on Budgets

Housing and Utilities

Housing is typically the largest monthly expense. Rising rent, mortgage payments, and property costs have increased financial pressure across income levels.

Utility bills have also become less predictable. Electricity, heating, and water costs often fluctuate with energy markets, making budgeting more difficult.

For many households, housing now consumes a larger share of income than it did just a few years ago.

Energy and Transportation

Energy costs influence daily spending more directly than most other expenses.

When fuel prices increase, households often respond quickly by adjusting behavior.

Common changes include:

- Driving less frequently

- Delaying travel

- Reducing discretionary spending

Transportation costs also raise the price of goods and services, spreading the impact of energy inflation throughout the economy.

Food and Healthcare

Food and healthcare expenses are essential and difficult to reduce.

These categories create consistent pressure on budgets because they are recurring and often unpredictable. When these costs rise, households typically reduce spending in other areas.

This pattern explains why retail and entertainment spending often slows during periods of higher living costs.

---

Practical Ways Households Adjust Their Budgets

Persistent cost increases have led to lasting changes in financial behavior. Many households now focus more on stability and risk management than on consumption.

Delaying Major Purchases

Large purchases are often postponed when budgets tighten.

Examples include:

- Replacing vehicles

- Renovating homes

- Buying new electronics

- Planning vacations

Delaying purchases helps preserve savings and reduce financial strain.

Building Larger Emergency Funds

Financial uncertainty encourages households to increase savings.

Common strategies include:

- Setting aside funds for unexpected expenses

- Automating monthly savings contributions

- Tracking spending more carefully

- Reducing nonessential purchases

These steps create financial flexibility and reduce reliance on credit.

Managing Debt More Carefully

Higher interest rates and rising living costs make debt management more important.

Households increasingly prioritize:

- Paying down high-interest balances

- Avoiding unnecessary borrowing

- Reviewing loan terms regularly

This approach supports long-term financial stability.

---

Risks and Limitations Households Should Monitor

Persistent cost pressures create financial risks that require attention. Monitoring these risks helps households respond early and avoid long-term problems.

Slower Discretionary Spending

When essential expenses rise, discretionary spending declines.

Industries most affected include:

- Retail

- Travel

- Dining

- Entertainment

Reduced spending in these sectors can slow job growth and economic expansion.

Widening Spending Inequality

Higher-income households usually have more savings and financial flexibility. They can maintain spending despite rising costs.

Lower-income households often face tighter budgets. They are more likely to reduce spending significantly when expenses increase.

This difference can widen economic inequality over time.

Ongoing Financial Stress

Financial stress increases when income growth fails to keep pace with expenses.

Warning signs include:

- Declining savings balances

- Rising credit card debt

- Late payments

- Increased reliance on borrowing

Recognizing these signals early allows households to adjust spending before problems escalate.

---

How to Build a Resilient Budget in a High-Cost Environment

Adapting to higher living costs requires consistent planning. The goal is not to eliminate expenses but to manage them effectively.

Practical steps include:

- Prioritize essential expenses

- Maintain a dedicated emergency fund

- Review recurring subscriptions regularly

- Adjust savings targets as costs change

- Plan for future price increases

These habits improve financial resilience and reduce uncertainty.

Households that review budgets regularly are better prepared to handle unexpected expenses and economic changes.

---

Conclusion: Stable Budgets Depend on Long-Term Planning

Rising living costs have reshaped household budgeting in lasting ways. The challenge is no longer temporary inflation but sustained pressure on essential expenses.

The most effective response is proactive planning. Households that monitor spending, build savings, and manage debt carefully are better positioned to maintain stability.

Looking ahead, the key factors to watch include wage growth, housing costs, and energy prices. These trends will determine whether financial pressure eases or continues in the years to come.

---

FAQ — Rising Living Costs and Household Budgets

Why do household budgets feel tight even when inflation slows?

Inflation may slow, but prices usually remain elevated. Households adjust to higher baseline costs rather than returning to previous spending patterns.

Which expenses affect household budgets the most?

Housing, energy, food, and healthcare typically create the most pressure because they are essential and difficult to reduce.

How can households prepare for rising living costs?

Building emergency savings, reducing discretionary spending, managing debt, and reviewing budgets regularly can improve financial stability.

When should households adjust their budgets?

Budgets should be reviewed whenever major expenses change, income shifts, or inflation increases the cost of essential goods and services.

---