Markets

S&P 500 Sectors: What’s Driving Returns in 2025 and How to Get Exposure

A Deep Dive into the Sector Rotation Behind U.S. Equity Returns — and How to Ride It

As of October 8, 2025, the S&P 500 continues to notch record highs, powered by a mix of robust corporate earnings and selective sector leadership.

Beneath the surface, however, the picture is anything but uniform. Some sectors have pulled far ahead, while others lag — a pattern shaped by the interplay of macroeconomic factors, valuation dynamics, and profit trends.

For intermediate investors, understanding these forces is key to adjusting exposure without overreaching.

produto:The Art of X: Build a Business That Makes You $100/Day

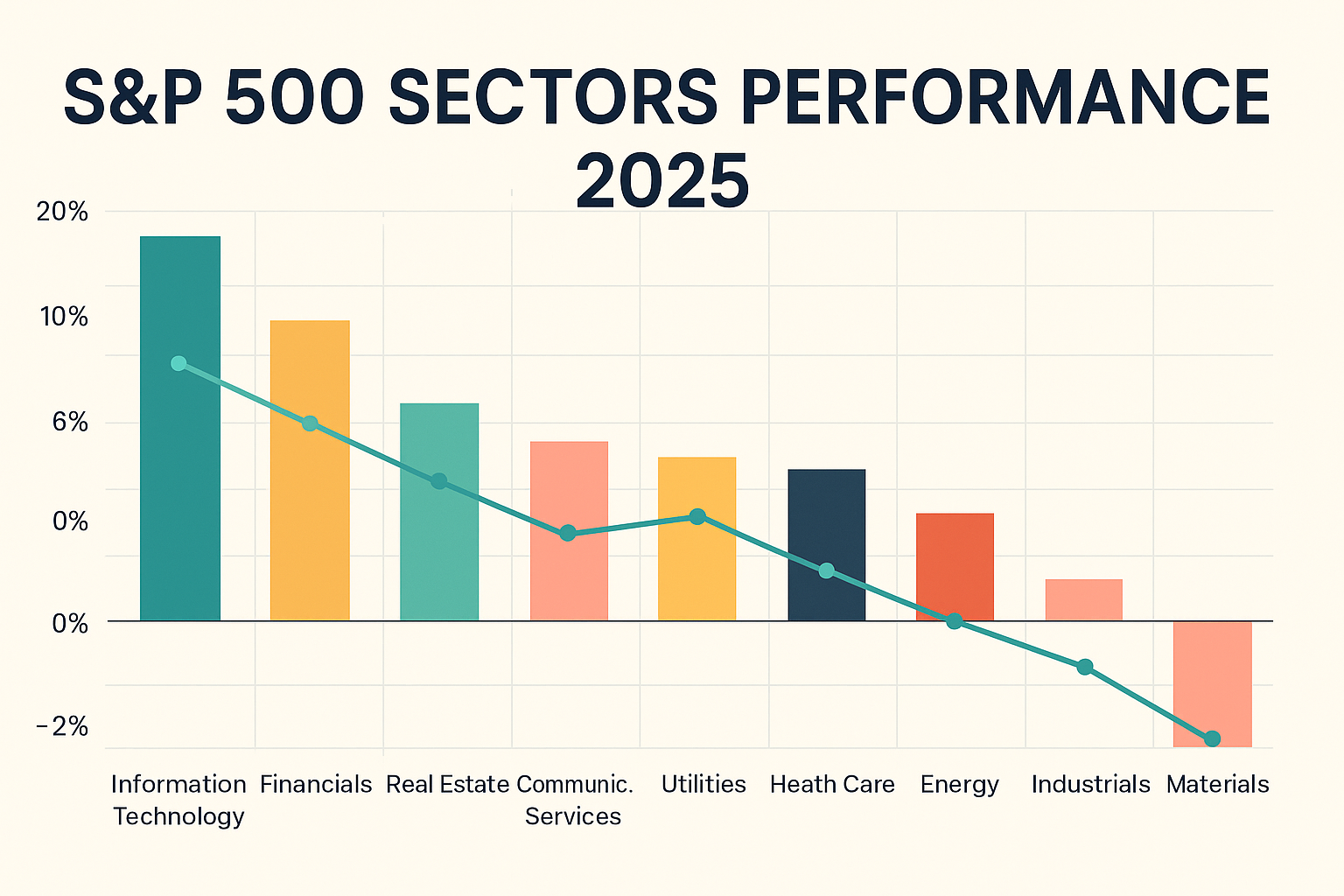

Sector Returns in 2025: Leaders and Laggards

- ### Q1 2025: Defensive and Energy Outperformance

In the first quarter of 2025, the S&P 500 posted a roughly –4.6% decline.

Within that weakness, however, defensive and energy sectors fared better than the broader market. Energy, in particular, managed a modest positive return even as cyclicals and tech stocks pulled back.

- ### Year-to-Date Through Mid-2025: A Split Market

By mid-2025, S&P Global’s sector dashboard revealed a widening dispersion across sectors.

Financials, Real Estate, and Communication Services posted consistently positive monthly returns, while Consumer Discretionary and Materials struggled with heightened volatility.

More than half of the S&P 500’s total returns through September stemmed from earnings growth rather than multiple expansion — a healthy sign for fundamentals-driven performance.

- ### Multi-Year View: Five-Year Cumulative Returns

Looking at five-year cumulative sector data underscores the divergence.

Energy and Financials have outperformed the aggregate index in several rolling periods, while other cyclical sectors show less runway ahead. This long-term perspective helps investors identify sectors that may already be “mid-cycle” versus those with more room to run.

---

Drivers Behind Sector Performance

- ### Earnings Growth and Margins

A central driver of sector performance in 2025 is earnings momentum.

Forward 12-month S&P 500 EPS estimates hover near $292, reflecting roughly 7.4% growth year-to-date through September 12, 2025, according to Carson Group.

Operational earnings remain the backbone of this year’s market advance, with cyclical sectors such as Financials, Industrials, and Materials positioned to benefit — provided macro conditions stay supportive.

- ### Macroeconomic Tailwinds and Headwinds

Interest Rates and Inflation

With interest rates still elevated and inflation sticky, capital-intensive sectors continue to face higher financing costs. Conversely, sectors with stable cash flows — such as Utilities and Consumer Staples — retain their defensive appeal.

J.P. Morgan noted earlier in the year that technology valuations had outpaced forward EPS projections, suggesting that some of the sector’s gains still depend on optimistic earnings expectations.

Trade Policy and Tariffs

Tariff volatility remains a wildcard. Policy shifts can hit export-driven industries — particularly Materials, Energy, and Industrials — and accelerate sector rotations as investors reprice risk. The CME Group highlights that this rotation pattern reflects heightened sector-specific exposure to trade shocks.

Capital Flows and Valuation

In 2025, investors are increasingly pursuing “narrow-slice” exposures instead of broad-market bets, amplifying flows into and out of sector ETFs.

Sectors trading at attractive valuations with solid momentum tend to capture inflows, a dynamic captured by the S&P 500 High Momentum Value Sector Rotation Index.

Structural Themes

- Artificial Intelligence and Technology remain dominant forces, especially for firms translating AI into tangible revenue growth.

- Energy Transition and Green Commodities continue to boost Materials and Renewable Energy players.

- Healthcare and Biotechnology sectors act as diversifiers amid regulatory or macro uncertainty.

---

How Investors Can Gain Sector Exposure

- ### Popular Sector ETFs

One of the most direct ways to gain exposure is through Select Sector SPDR ETFs — for example, XLF for Financials, XLK for Technology, and XLE for Energy.

Vanguard and iShares also offer sector ETFs, often with lower fees or thematic variations.

In practice, many portfolio managers allocate 10–30% of capital to sectors with offensive or defensive traits based on macro outlooks.

- ### Systematic Rotation Strategies

Intermediate investors may apply systematic rules — such as shifting exposure once a sector’s relative momentum surpasses a predefined threshold — or use more advanced quantitative overlays.

The goal is to capture rotation effects without relying on perfect timing.

Crucially, these strategies should include exit points, drawdown limits, and periodic rebalancing.

- ### Risks and Pitfalls

- Overconcentration: Heavy bets on one sector magnify scenario risk.

- Poor Timing: Late shifts often miss the move.

- Transaction Costs and Taxes: Frequent trades erode net returns.

- Theme Decay: Today’s strong sector can weaken abruptly due to regulation, disruption, or macro shifts.

---

Outlook for Late 2025 and Beyond

- ### Earnings Outlook and Growth Trends

Goldman Sachs projects roughly 7% EPS growth for both 2025 and 2026, suggesting that fundamentals still have fuel — assuming stable rates and inflation.

Barclays recently raised its year-end 2025 S&P 500 target to 6,450, citing stronger-than-expected earnings momentum.

- ### Sectors Best Positioned — and Those at Risk

Technology and innovation-driven industries, Financials (in favorable spread environments), and stable Consumer sectors appear well positioned for the second half of the year.

By contrast, Basic Materials, Consumer Discretionary, and certain cyclical segments may remain vulnerable to macro shocks.

- ### Rotation Risks That Could Reverse Trends

- A more aggressive Federal Reserve rate path

- Inflation surprises above expectations

- Sudden trade or regulatory shifts

- Unexpected corporate earnings deceleration

produto:The Art of X: Build a Business That Makes You $100/Day

Conclusion and Key Takeaways

- In 2025, sector rotation has been a defining feature of market dispersion.

- Earnings growth — not just multiple expansion — remains the core driver of returns.

- ETFs and disciplined rotation strategies can help capture trends, but managing concentration and timing risks is essential.

- Looking ahead, sectors with solid fundamentals and exposure to structural themes have the most potential runway — though macro volatility could quickly reshape the landscape.

---

FAQ

Q: Should I try to time sector switches midyear?

A: Exact timing is risky. A steadier approach is periodic rebalancing and using momentum filters to avoid emotional decisions.

Q: Do sector ETFs carry more risk than broad-market funds like SPY?

A: Yes — they’re less diversified. When a sector underperforms, losses can be sharper. Position sizing and exposure limits are key.

Q: How often should I review or rebalance sector tilts?

A: Many investors choose quarterly or semiannual reviews. This cadence captures longer cycles and reduces excessive trading.

Q: Can a lagging sector early in 2025 recover later?

A: Absolutely. Leadership reversals often occur as macro cycles shift. Maintaining a mix of offensive and defensive exposure can be prudent.

---

Sources and Further Reading

- Carson Group, U.S. Equity Earnings Outlook, September 2025

- S&P Global, Sector Dashboard, July 2025

- J.P. Morgan, Equity Strategy Brief, March 2025

- CME Group, Sector Rotation and Trade Policy Risk, 2025

- Goldman Sachs, Equity Research: 2025–2026 Earnings Outlook

- Barclays, S&P 500 Year-End Targets Update, September 2025

---