Personal Finance

Student Loan Repayment Changes 2026: What to Do Next

Understand new repayment rules and protect your monthly budget

Many borrowers are unsure what happens to their student loans after the SAVE plan ended in 2026. The biggest concern is simple: Will my monthly payment increase, and what do I need to do now?

This guide explains the new repayment rules, the key deadlines to know, and the practical steps you can take to manage your payments and protect your finances. Whether you rely on income-driven repayment or are planning long-term loan forgiveness, understanding these changes is essential for budgeting in 2026 and beyond.

---

What Changed in 2026: The End of the SAVE Plan

The most important shift is structural. The Saving on a Valuable Education (SAVE) repayment plan was formally terminated in March 2026 following a federal court settlement.

Soon after, the U.S. Department of Education issued transition guidance on 03/27/2026 directing loan servicers to move affected borrowers into alternative repayment options.

This change is permanent. It resets how millions of federal student loan borrowers repay their debt.

Key Dates to Know

- 03/2026 — SAVE plan formally ended

- 03/27/2026 — Federal transition guidance issued

- 04/2026 — Borrower notices began arriving

- 07/01/2026 — 90-day repayment selection period begins

- Late 2026 — New payment levels begin affecting household budgets

About 7.5 million borrowers must now choose a new repayment plan or be placed automatically into a standard repayment schedule.

That decision directly affects monthly costs, interest paid over time, and eligibility for forgiveness programs.

---

How the Repayment Transition Works

Understanding the process helps reduce stress and prevent costly mistakes. The transition follows a clear sequence.

Once your loan servicer sends a formal notice, you will have a limited window—typically about 90 days—to select a repayment option.

If you do nothing, the system assigns a default plan.

Step-by-Step Transition Process

- Receive an official notice from your loan servicer

- Review available repayment plan options

- Choose a plan before the deadline

- Begin payments under the new structure

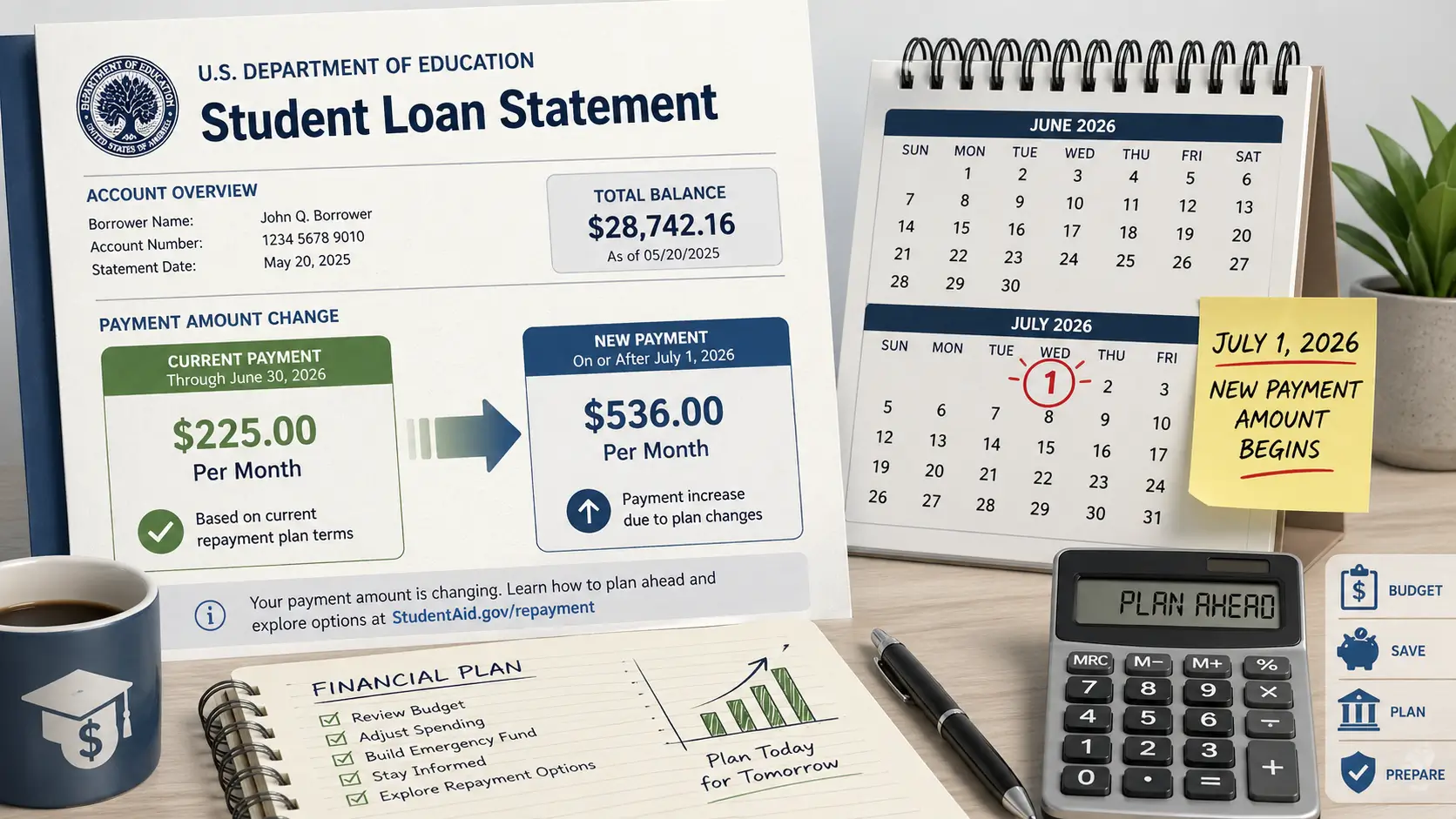

The critical date is 07/01/2026, when loan servicers begin issuing mandatory transition notices nationwide.

Missing the deadline usually results in automatic placement into a standard repayment plan, which often means higher monthly payments.

---

How Payments and Forgiveness May Change

For many borrowers, the SAVE plan offered the lowest possible monthly payment. Moving to a different repayment structure can increase required payments and change the timeline for loan forgiveness.

Common Financial Changes

- Higher monthly payments

- Different eligibility rules for forgiveness

- Longer repayment timelines

- Higher total interest costs

- Increased risk of missed payments

The size of the change depends on three factors:

- Income level

- Loan balance

- Repayment plan selected

Borrowers with tight budgets may feel the impact quickly. Even a moderate increase in payments can affect savings, spending, and financial stability.

---

Practical Steps to Manage Your Student Loan Payments

Preparation is the most effective way to reduce financial risk during the transition. Small actions taken early can prevent larger problems later.

Actions to Take Now

Review your loan information

Check your current balance, interest rate, and payment history.

Estimate your future payment

Ask your loan servicer for a payment estimate under different repayment plans.

Compare affordability, not just monthly cost

Look at total repayment time, interest, and flexibility.

Build a small emergency buffer

Saving one or two months of payments can provide protection during the transition.

These steps turn uncertainty into a manageable financial plan.

---

Risks to Watch During the Transition

Most borrowers will navigate the transition successfully. However, several risks are worth monitoring.

Key Risks

Payment shock

A sudden increase in monthly payments can strain your budget.

Missed deadlines

Failing to select a repayment plan may result in automatic enrollment in a higher-cost structure.

Credit score damage

Late or missed payments can reduce credit scores and increase borrowing costs.

Reduced financial flexibility

Higher payments may limit your ability to save or handle emergencies.

These risks are manageable when borrowers understand the rules and act early.

---

How Student Loan Changes Affect Household Budgets

Student loan payments function like rent, insurance, or utilities. When they increase, households often adjust spending elsewhere.

Common adjustments include:

- Cutting discretionary spending

- Delaying large purchases

- Increasing use of credit

- Slowing savings growth

Treating the repayment transition as a predictable budget change—not a sudden surprise—helps maintain financial stability.

---

Conclusion: Plan Early to Stay in Control of Your Payments

The 2026 student loan repayment changes mark a lasting shift in how federal loans are managed.

The key takeaway is practical: your repayment structure may change, and preparation determines the outcome.

Review your options early, estimate your future payments, and build a plan that fits your budget. Taking action before deadlines arrive reduces stress, protects your credit, and supports long-term financial stability.

As repayment rules continue to evolve, borrowers who treat student loans as part of a structured financial plan will be better prepared for future changes.

---

FAQ

When did the SAVE repayment plan end?

The SAVE plan officially ended in March 2026 following a federal court settlement. Borrowers must transition into new repayment plans during 2026.

What is the most important student loan deadline in 2026?

Loan servicers begin issuing mandatory transition notices on July 1, 2026. Borrowers typically have about 90 days to choose a new repayment plan.

Will my student loan payment increase after the SAVE plan ends?

Many borrowers will see higher monthly payments, but the exact amount depends on income, loan balance, and the repayment option selected.

What happens if I do not choose a repayment plan?

If no plan is selected, borrowers are usually automatically placed into a standard repayment schedule, which often results in higher payments.

---