Economy

The Hidden Stress Signal in U.S. Consumers

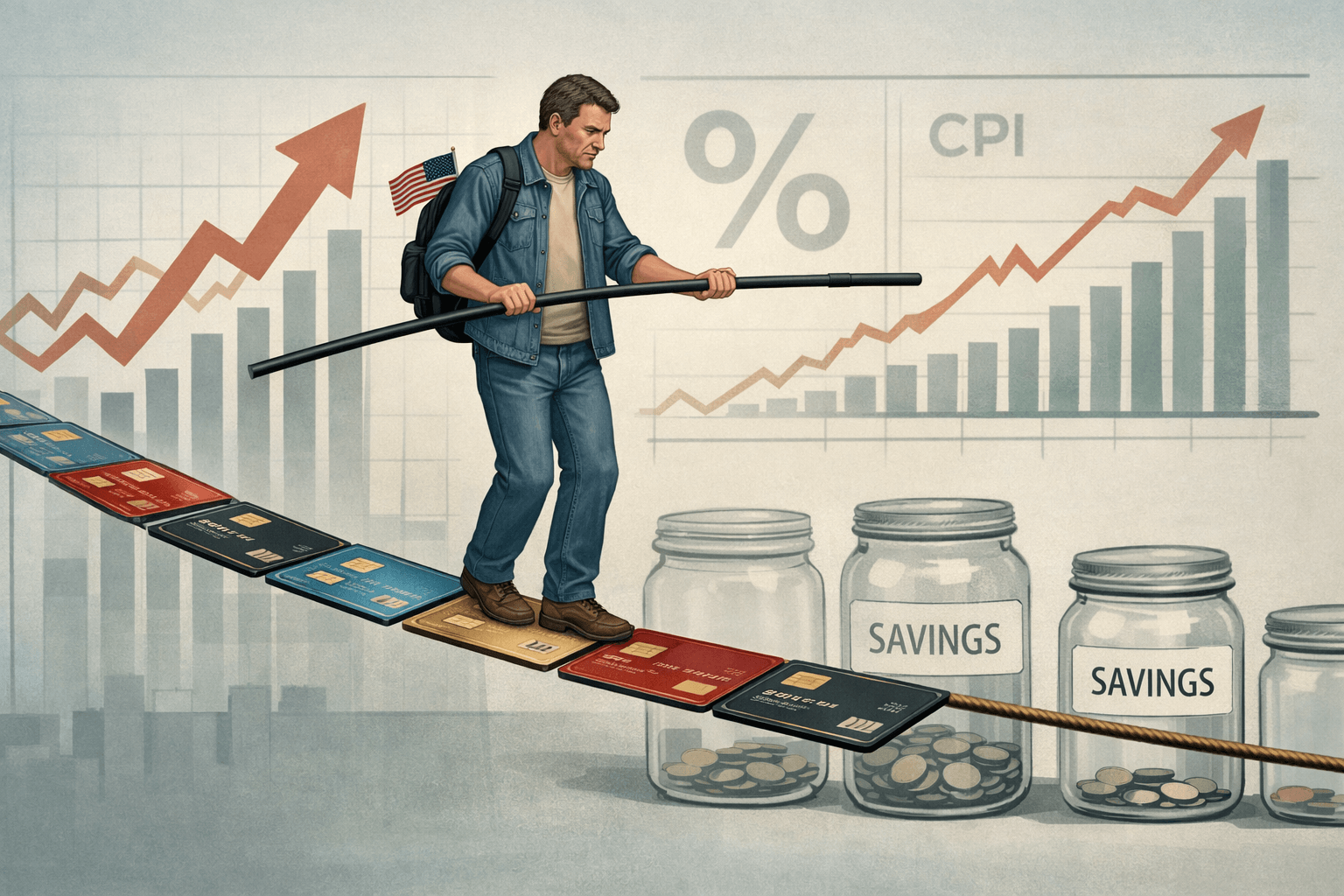

Falling savings and rising debt suggest a fragile foundation beneath steady spending

The U.S. consumer still looks strong—at least on the surface. Stores are busy, travel demand persists, and spending hasn’t collapsed. But a closer look reveals something more unsettling: Americans aren’t necessarily earning their way through this economy anymore—they’re borrowing their way through it.

That shift is subtle, but it may be one of the most important economic signals of early 2026.

Spending Is Holding—But the Foundation Is Cracking

As of January 2026, the personal savings rate has fallen below 4.0%, near its lowest level in years. At the same time, inflation—still running at 3.2% year-over-year in February 2026—continues to chip away at real income.

Yet spending hasn’t dropped proportionally. Why?

Because households are increasingly leaning on credit. U.S. credit card balances climbed past $1.1 trillion in Q4 2025, with data released in February 2026 confirming a steady rise in delinquency rates.

This creates a fragile dynamic: consumption appears stable, but it’s being sustained by debt rather than financial strength. And that distinction matters.

The Squeeze From Rates and Prices

The pressure isn’t coming from one direction—it’s coming from both.

On one side, prices remain elevated. On the other, borrowing has become significantly more expensive. The Federal Reserve has kept interest rates above 5.25% as of March 19, 2026 (ET), reinforcing tight financial conditions across the economy.

For households, that means higher credit card interest, more expensive loans, and less flexibility. Over time, this erodes the cushion that once supported spending resilience.

The result? Consumers are still moving—but with less margin for error.

Why Markets Are Paying Attention Now

This is where the signal turns critical.

Consumer spending drives roughly two-thirds of U.S. economic activity. If that engine begins to slow—not abruptly, but gradually—the effects can ripple quickly through corporate earnings, hiring trends, and market sentiment.

Early 2026 growth expectations are already softening, reflecting weaker discretionary demand. Companies tied to consumer spending are starting to feel the pressure, even if headline data hasn’t fully turned.

For the Federal Reserve, the dilemma is sharpening: keep policy tight to fight inflation, or risk pushing an already strained consumer too far.

The real story isn’t that consumers are breaking—it’s that they’re stretching. And history suggests that stretch rarely lasts forever.

---

FAQ

Why is the savings rate important right now?

A lower savings rate means households have less financial buffer, making them more vulnerable to economic shocks.

Is rising credit card debt always a bad sign?

Not always, but rapid increases—especially alongside rising delinquencies—can signal financial stress.

How does this affect the broader economy?

If consumers pull back spending, it can slow GDP growth and pressure corporate earnings.

Could this lead to a recession?

It’s not definitive, but weakening consumer fundamentals often precede broader economic slowdowns.

---

Sources and Further Reading

- U.S. Personal Income and Outlays — Bureau of Economic Analysis — 02/28/2026 — https://www.bea.gov/

- Household Debt and Credit Report — Federal Reserve Bank of New York — 02/2026 — https://www.newyorkfed.org/

- Consumer Price Index Summary — Bureau of Labor Statistics — 03/12/2026 — https://www.bls.gov/

- FOMC Statement — Federal Reserve — 01/29/2026 — https://www.federalreserve.gov/

- U.S. Economic Outlook Update — Congressional Budget Office — 02/2026 — https://www.cbo.gov/

---