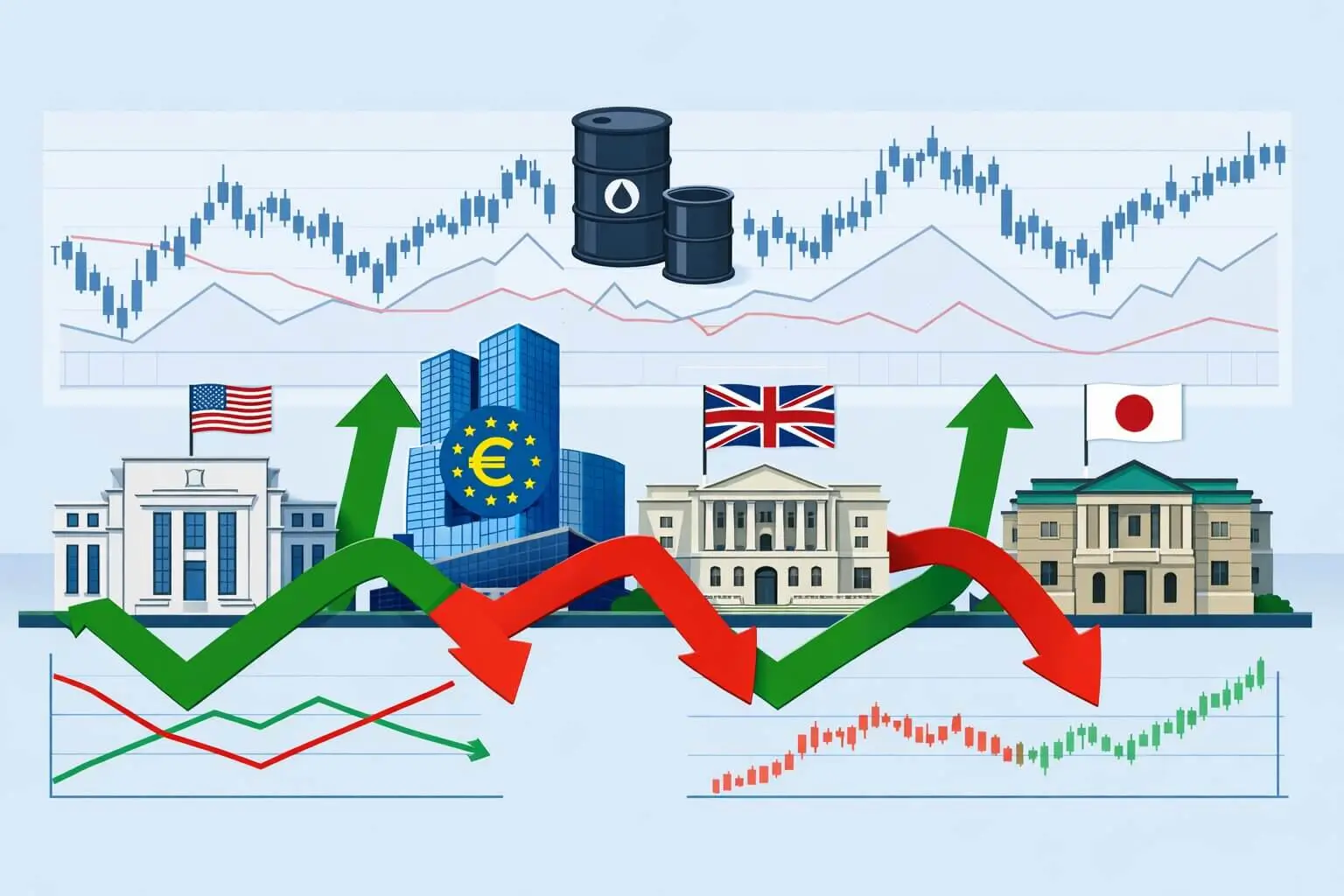

Global interest rates are no longer drifting toward an easy 2026 easing cycle.

The expected path has changed. On 04/29/2026, the Federal Reserve kept its target range at 3.50%–3.75%, while warning that inflation remains elevated and global energy prices are adding uncertainty. One day later, on 04/30/2026, the European Central Bank held its deposit facility rate at 2.00%, its main refinancing rate at 2.15%, and its marginal lending facility at 2.40%.

The Bank of England also held Bank Rate at 3.75% on 04/30/2026, but the vote showed a different risk: one policymaker wanted an immediate increase to 4.00%, not a cut. Japan remains the outlier in the opposite direction. The Bank of Japan kept rates at 0.75% in April, but pressure for another hike is rising as inflation and bond yields climb.

The result is a sharper global turning point than the original 2026 rate-cut narrative suggested. Central banks are not just waiting to cut. Some are now asking whether policy is tight enough.

Why This Matters Again Now

The update matters because the rate debate has moved from “when do cuts start?” to “what if cuts do not arrive in 2026?”

A Reuters poll conducted from 05/14/2026 to 05/19/2026 found that 83 of 101 economists expected the Fed to keep rates unchanged through the third quarter. The same report said the 10-year Treasury yield had moved above 4.6%, a level that directly affects mortgage rates, corporate borrowing costs, equity valuations, and fixed-income returns.

That changes the practical consequence for readers. A delayed easing cycle means households may face higher refinancing costs for longer, businesses may delay investment, and investors may need to rethink portfolios built around falling yields.

The Global Policy Pause Is No Longer Neutral

A pause can mean two different things.

In early 2026, it looked like a bridge toward rate cuts. By May 2026, it looks more like a defensive position against renewed inflation risk.

The Fed’s April statement pointed directly to global energy prices as part of the inflation problem. The ECB said the Middle East war had pushed energy prices higher and increased both upside inflation risks and downside growth risks. The Bank of England said UK CPI inflation had increased to 3.3% and warned that second-round effects in wages and pricing could require policy to lean against inflation.

That is the new dilemma. Growth is not strong enough to make central banks comfortable. But inflation is not weak enough to let them ease quickly.

For markets, this creates a less forgiving setup. If inflation cools, bond yields could fall and risk assets may regain support. If inflation stays sticky, investors could face higher yields, tighter financial conditions, and weaker valuation multiples at the same time.

Japan Is Still Moving Against the Cycle

Japan’s role is increasingly important because the Bank of Japan is not debating rate cuts.

The BOJ held its policy rate at 0.75% in April 2026, but Reuters reported that three policymakers dissented in favor of a hike to 1.00%. That is a major shift for an economy that spent decades anchored near zero rates.

This matters beyond Japan. Higher Japanese yields can affect global capital flows because Japanese investors have long been major buyers of foreign bonds. If domestic yields become more attractive, more capital may remain in Japan or return home.

That could reduce demand for foreign bonds and add pressure to global yields. It could also support the yen if markets believe the BOJ is moving toward further tightening.

For investors, Japan is no longer just a low-rate exception. It is becoming one of the pressure points in the global bond market.

What It Means for Markets and Borrowers

The global interest-rate turning point affects four areas most directly.

First, borrowing costs may stay high. Mortgage rates, auto loans, credit cards, corporate debt, and refinancing costs all respond to rate expectations and bond yields. A slower path to cuts means less relief for consumers and companies.

Second, equity valuations face a tougher test. Higher yields increase the discount rate applied to future earnings. That can hurt long-duration growth stocks most, especially if earnings expectations also weaken.

Third, fixed income becomes more attractive but more volatile. Higher yields improve income potential, but bond prices remain vulnerable if inflation surprises again or central banks sound more hawkish.

Fourth, currency markets may become more unstable. If the Fed holds longer while the ECB stays cautious and the BOJ moves toward hikes, interest-rate differentials could shift quickly. That matters for multinational earnings, import prices, and emerging-market capital flows.

What to Watch Next

The next signal is inflation breadth.

Energy-driven inflation can be temporary if oil and fuel prices reverse. It becomes more dangerous if it spreads into wages, services, transportation, rents, and inflation expectations. That is why central banks are watching second-round effects so closely.

The Fed’s next major test is whether inflation data justifies keeping an easing bias in place. The Bank of England’s next decision on 06/18/2026 will show whether the April dissent for a hike was isolated or the start of a more hawkish shift. The BOJ’s next meetings will test whether Japan’s bond-market pressure turns into another rate increase.

For now, the global rate cycle has reached a more fragile phase. The risk is no longer just that rate cuts arrive later. The bigger risk is that markets priced for relief may have to adjust to a world where global interest rates stay restrictive for longer.

FAQ

Why are global interest rates at a turning point in 2026?

Global interest rates are at a turning point because central banks are delaying cuts while energy-driven inflation risks increase. The Fed, ECB, Bank of England, and Bank of Japan are all signaling caution rather than a synchronized easing cycle.

What did the Federal Reserve do in April 2026?

The Federal Reserve kept the federal funds target range at 3.50%–3.75% on 04/29/2026. Its statement said inflation remained elevated and that Middle East developments were contributing to uncertainty.

Why is the Bank of Japan different from other central banks?

The Bank of Japan is still normalizing policy after decades of ultra-low rates. It held rates at 0.75% in April 2026, but dissenting policymakers favored a hike to 1.00%, showing pressure for further tightening.

How could delayed rate cuts affect investors?

Delayed rate cuts could keep bond yields high, pressure equity valuations, increase borrowing costs, and create more volatility in currency markets. Fixed-income investors may benefit from higher yields, but inflation surprises could still hurt bond prices.

Sources and Further Reading

- Federal Reserve Issues FOMC Statement — Federal Reserve — 04/29/2026 — https://www.federalreserve.gov/newsevents/pressreleases/monetary20260429a.htm

- Monetary Policy Decisions — European Central Bank — 04/30/2026 — https://www.ecb.europa.eu/press/pr/date/2026/html/ecb.mp260430~81b7179e6f.en.html

- Bank Rate Maintained at 3.75% — Bank of England — 04/30/2026 — https://www.bankofengland.co.uk/monetary-policy-summary-and-minutes/2026/april-2026