The best personal loans of 2026 share three traits: low APRs relative to credit cards, no origination fees, and loan ceilings high enough for serious consolidation. Average personal loan rates landed at 12.27% as of 05/13/2026, according to Bankrate Monitor data — nearly 10 percentage points below the 21.52% average APR Americans pay on credit card balances assessed interest. For households juggling high-rate revolving debt, the fixed-rate personal loan math is the most attractive it has been since the Federal Reserve began holding its policy rate at 3.50%–3.75% in December 2025.

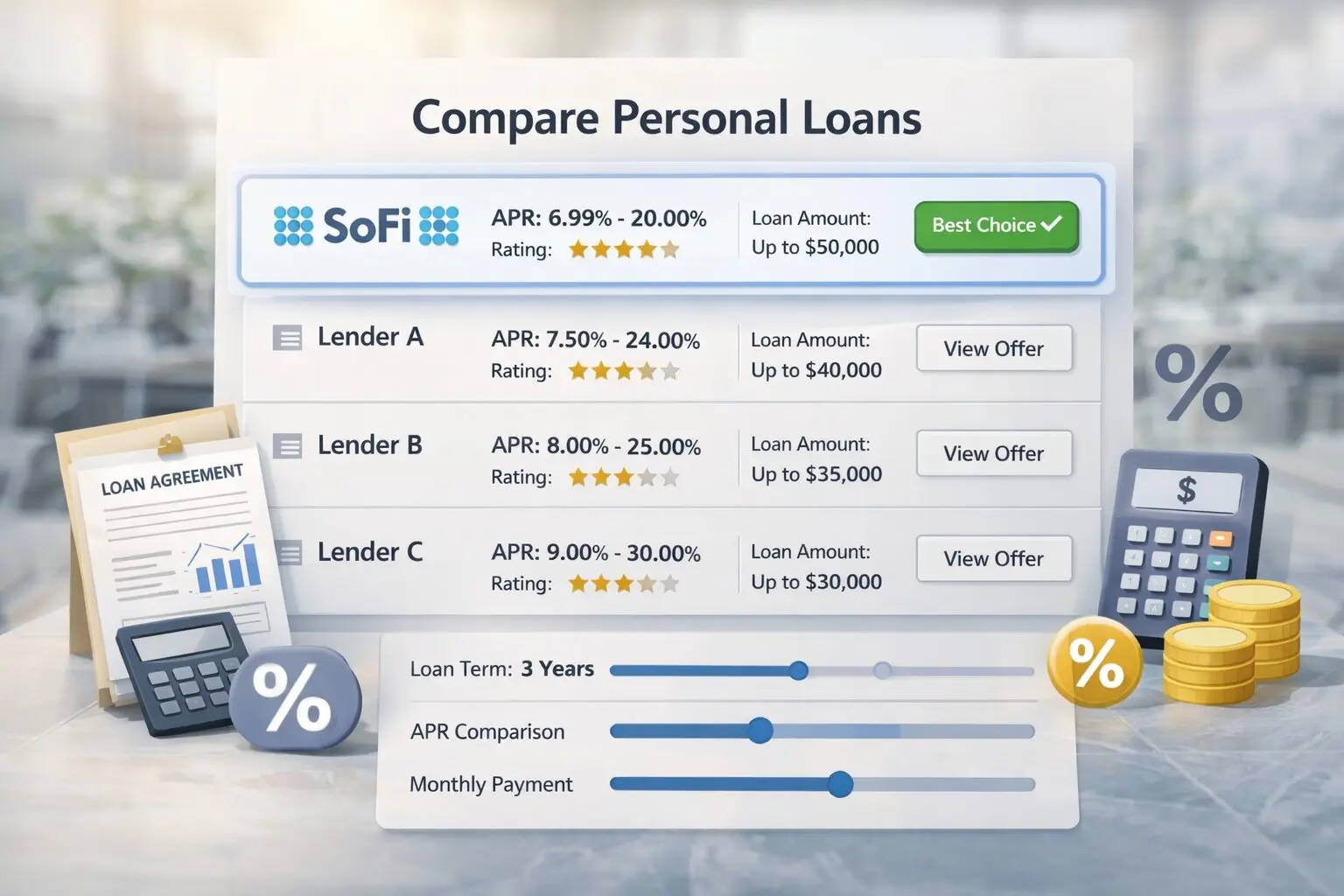

But not every lender offers the same trade-off. APR floors, origination fees, maximum loan size, and underwriting flexibility vary widely — and choosing wrong can cost borrowers thousands over a five-year term. Among the lenders most relevant to U.S. consumers in 2026, four stand out: SoFi, LightStream, Upstart, and Discover. SoFi remains the strongest all-around option for prime borrowers seeking larger loans without fees.

Personal Loans in 2026: A Costly Credit Market

Total U.S. household debt reached $18.8 trillion in Q1 2026, according to the Federal Reserve Bank of New York's Quarterly Report on Household Debt and Credit released 05/12/2026 — a record, driven primarily by mortgage and auto balances. Credit card balances actually fell by $25 billion to $1.252 trillion, the typical post-holiday seasonal dip, but the average APR on accounts assessed interest still sat at 21.52% in Q1 2026 per Federal Reserve G.19 data.

That gap between revolving APRs and fixed personal loan rates is the central reason demand for consolidation loans has remained durable through the Fed's pause cycle.

Common personal loan use cases in 2026 include consolidating high-interest credit card balances, financing home renovations and major purchases, covering medical bills or emergency expenses, and refinancing existing high-rate installment debt.

Unlike credit cards, personal loans feature fixed APRs and structured monthly payments. That makes total interest cost predictable from the first payment to the last.

Why This Matters Again Now

The April 29, 2026 FOMC meeting marked the third consecutive hold of the federal funds rate at 3.50%–3.75% — but the decision was the most contested in over three decades. The Committee split 8-4, with Governor Stephen Miran favoring a 25-basis-point cut and three regional presidents opposing the statement's continued easing bias. Following the announcement, CME Group's FedWatch tool briefly showed traders pricing non-zero odds of a Fed rate hike at the December 2026 meeting.

The practical takeaway: the window of "rates may come down soon" is closing. Annual U.S. inflation reached 3.8% in April 2026, well above the Fed's 2% target. For borrowers waiting to refinance high-rate credit card debt at a lower personal loan APR, "wait and see" is now a bet against the Fed's own communicated path.

What Defines a Competitive Personal Loan in 2026

Loan Size and Terms

Most major lenders offer personal loans between $1,000 and $100,000, with repayment terms of two to seven years. Higher ceilings matter most for consolidation strategies that aim to roll multiple high-interest balances into a single installment.

APR Structures

As of 05/13/2026, the Bankrate average personal loan APR was 12.27% for a borrower with a 700 FICO score, $5,000 loan, and three-year term. Longer five-to-seven-year terms typically carry meaningfully higher APRs — often 4 to 6 percentage points above three-year rates — because the lender carries duration risk longer.

For excellent-credit borrowers, the lowest advertised rates among Bankrate-tracked lenders started near 6% in May 2026, with LightStream, LendingClub, and Upstart all offering sub-7% floors.

Approval Criteria

Most digital lenders weigh FICO score and credit history length, verified income and employment stability, debt-to-income ratio (typically under 50%), and payment history across active accounts.

Borrowers with FICO scores above 700 generally qualify for the lowest advertised rates. Below 680, available APRs climb sharply — often above 20%.

Best Personal Loan Lenders in the U.S. for 2026

SoFi — Best Overall for Larger Loans

Loan amounts: $5,000 to $100,000 APR range: 7.74%–35.49% with all available discounts applied (autopay, direct deposit, debt consolidation) Repayment terms: 2 to 7 years Fees: None — no origination, late, or prepayment fees

SoFi's strongest case is for prime borrowers seeking larger loans. Its $100,000 ceiling matches LightStream and exceeds most digital lenders. The zero-fee structure is a meaningful differentiator: on a $20,000 loan, avoiding a 5% origination fee preserves $1,000 of borrower proceeds upfront. Same-day funding is available for approved applicants.

Cons: The $5,000 minimum shuts out small borrowers. The headline 7.74% floor requires stacking all three member discounts — autopay, direct deposit of $1,000+ monthly to a SoFi checking account, and using the loan for debt consolidation with SoFi paying creditors directly. Without those, the floor sits closer to 8.49%.

Borrowers can pre-qualify for a SoFi personal loan in minutes via a soft credit pull — no impact on FICO score.

LightStream — Best for Excellent Credit

Loan amounts: Up to $100,000 APR range: 6.49%–24.89% Fees: None Funding: Same-day available

LightStream, a division of Truist Bank, offers some of the lowest advertised APRs in the market for borrowers with strong credit profiles. Its Rate Beat Program promises to undercut any verified competitor offer by 0.10 percentage points. For home improvement borrowers, terms extend up to 20 years on qualifying loans.

Cons: No pre-qualification on LightStream's own site — borrowers commit to a hard credit pull at application. Underwriting is strict; thinner credit files are typically declined. There is no soft-pull option to test eligibility before committing.

Upstart — Best for Thin Credit Files

Loan amounts: $1,000 to $50,000 APR range: 6.20%–35.99% Underwriting: AI-driven, considers education and employment beyond FICO

Upstart's machine-learning model evaluates factors traditional underwriters ignore — degree, field of study, and work history — which broadens access for borrowers with limited credit. Funding typically lands within one business day.

Cons: Origination fees can reach 12% of the loan amount, materially raising true cost. Late fees apply. The headline 6.20% floor is reserved for the most creditworthy applicants — most borrowers see double-digit APRs.

Discover — Best for Predictable Repayment

Loan amounts: Up to $40,000 Fees: No origination fees Structure: Fixed APRs only

Discover targets borrowers who want stable, predictable repayment with no surprises. There are no origination fees and no prepayment penalties.

Cons: The $40,000 cap is too low for large consolidation strategies. Approval standards favor borrowers with established credit; no AI-based underwriting flexibility for borderline applicants.

Why SoFi Leads the Market in 2026

Among the four, SoFi's combination of scale, pricing, and member ecosystem makes it the most defensible overall choice for prime borrowers.

Higher loan ceiling: The $100,000 maximum supports large-scale consolidation that smaller-cap lenders like Discover and Upstart cannot match.

Competitive APR with stacked discounts: Prime borrowers who can meet all three discount criteria reach a 7.74% effective floor — well below the 12.27% national average and dramatically below the 21.52% credit card APR average.

Zero fees: No origination fee means a $30,000 loan delivers $30,000 to the borrower. That's a structural advantage over fee-charging competitors like Upstart, where a 6% origination fee on the same loan would deliver only $28,200.

Member ecosystem: Unemployment protection, career coaching, and integrated investment and banking products add value for borrowers who use multiple SoFi services.

For borrowers exploring consolidation or refinancing, checking a personalized rate with SoFi takes minutes and uses a soft credit pull — no impact on FICO score.

When a Personal Loan Makes Financial Sense

Debt Consolidation

The 21.52% credit card APR versus 12.27% personal loan APR gap means a borrower carrying $10,000 in revolving balances at 21.52% would save roughly $900–$1,200 annually in interest by refinancing — and substantially more for borrowers who qualify for sub-10% APRs.

Credit Card Refinancing

Borrowers with consistent income but multiple revolving balances benefit from converting variable-rate debt into a fixed-payment installment loan. Predictable monthly outflows simplify cash flow planning and create a defined payoff date.

Major Funded Expenses

Common uses include home renovations (often eligible for longer LightStream terms), medical procedures not covered by insurance, wedding or relocation costs, and emergency expenses where fast funding matters.

A personal loan is not the right tool for everyday discretionary spending or for borrowers without a clear repayment plan — the fixed monthly commitment becomes a burden if income is unstable.

What Borrowers Should Watch Through 2026

Federal Reserve path: The Fed held at 3.50%–3.75% for three consecutive meetings through 04/29/2026. The April statement flagged that "some policy firming would likely become appropriate if inflation were to continue to run persistently above 2%" — meaning the next move could be either direction. Borrowers waiting for rate cuts to lower personal loan APRs may wait through the rest of the year.

Lender underwriting tightening: Q1 2026 NY Fed data showed mortgage transitions into serious delinquency rising from 1.4% to 1.5%. If broader credit stress builds, lenders typically respond by raising minimum FICO thresholds and lowering maximum loan amounts.

Origination fee creep: Several fintech lenders have raised origination fees as funding costs have stayed elevated. Borrowers should compare APR inclusive of any origination fees — not headline interest rate alone.

For borrowers carrying high-rate credit card debt, locking in a fixed-rate personal loan in mid-2026 is more likely to be the better trade than waiting for Fed action that may not arrive. Prime borrowers can start a soft-pull rate check at SoFi to see what they qualify for today.

FAQ

What credit score is needed for a personal loan in 2026?

Most lenders require a FICO score of at least 650. The lowest advertised APRs — 6.20% to 7.74% — are typically reserved for borrowers with scores above 720 and low debt-to-income ratios.

Are personal loans better than credit cards for debt consolidation?

For borrowers carrying balances on credit cards averaging 21.52% APR, generally yes. A fixed-rate personal loan at the 12.27% May 2026 average APR would meaningfully reduce interest cost and add the benefit of a defined payoff date.

How quickly can a personal loan be approved and funded?

Pre-qualification with soft credit pulls takes minutes at SoFi, Upstart, and LightStream. Funding typically arrives within one to three business days; same-day funding is available with SoFi and LightStream for qualifying applicants.

What is the maximum personal loan available in the U.S.?

SoFi and LightStream both offer up to $100,000 for qualified borrowers. Upstart caps at $50,000, and Discover caps at $40,000.

Sources and Further Reading

- Household Debt Balances Rise Slightly as Delinquency Transition Rates Hold Steady (Q1 2026) — Federal Reserve Bank of New York — 05/12/2026 — https://www.newyorkfed.org/newsevents/news/research/2026/20260512

- Average Personal Loan Interest Rates in May 2026 — Bankrate — 05/13/2026 — https://www.bankrate.com/loans/personal-loans/average-personal-loan-rates/

- Fed Interest Rate Decision April 2026: Fed Holds Rates Steady Amid Dissent — CNBC — 04/29/2026 — https://www.cnbc.com/2026/04/29/fed-interest-rate-decision-april-2026.html

- Average Credit Card Interest Rate in US Today — LendingTree — 05/2026 — https://www.lendingtree.com/credit-cards/study/average-credit-card-interest-rate-in-america/

- SoFi 2026 Personal Loan Review — NerdWallet — 2026 — https://www.nerdwallet.com/reviews/loans/personal-loans/sofi-personal-loans

AlphaPulse may earn a commission from purchases made through links on this page. Our recommendations are based on independent analysis, and partnerships do not influence our editorial evaluation.