Where to park cash in 2026 is no longer a simple “highest APY wins” question. Short-term rates are still high enough to matter, but the best choice depends on taxes, liquidity, insurance, account size, and how soon the money may be needed.

The Fed held its target range at 3.50% to 3.75% on 04/29/2026, and short-term cash yields are still anchored near that policy range. That makes cash productive — but not all cash vehicles solve the same problem.

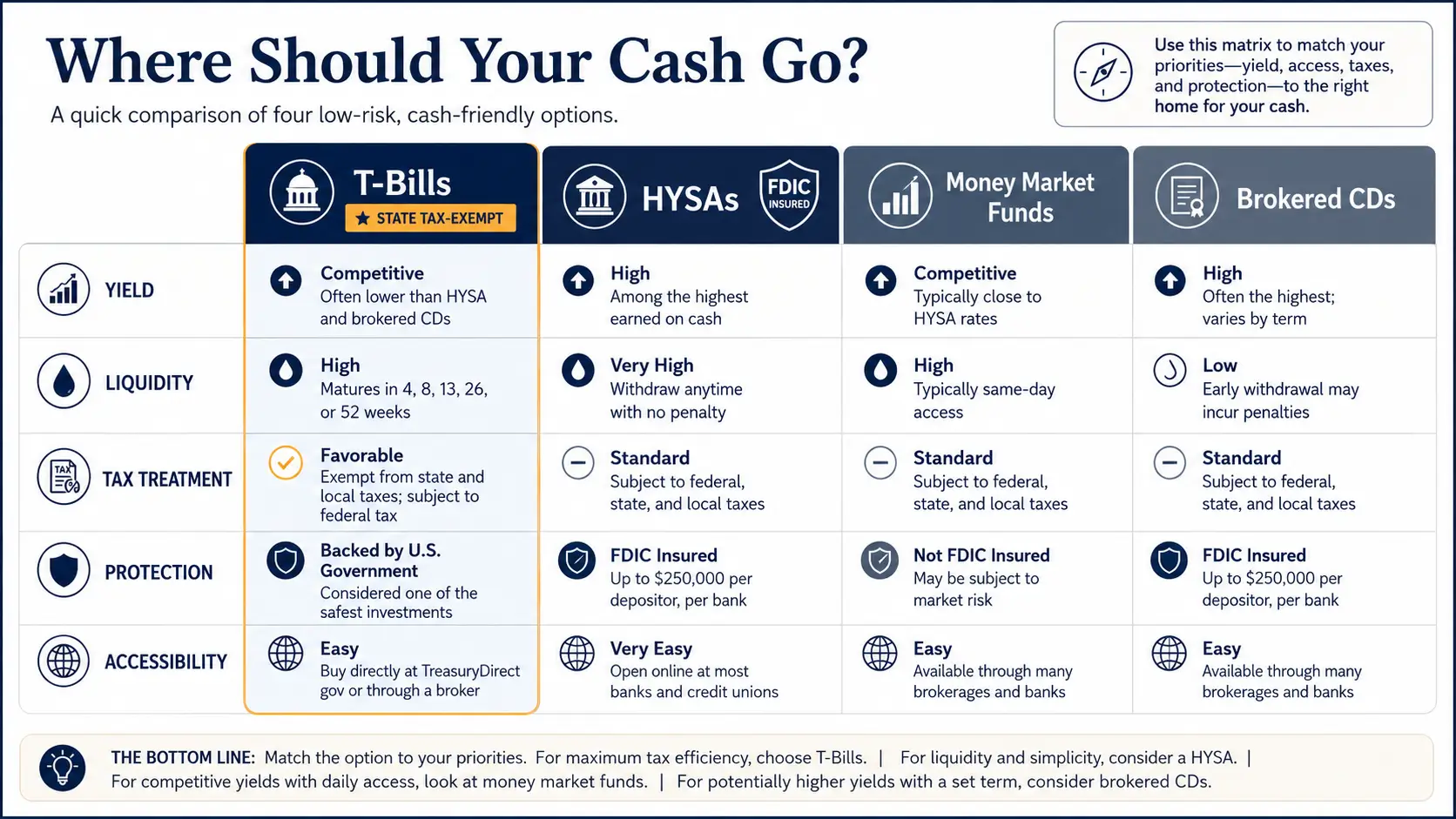

Where to Park Cash in 2026: The Decision Matrix

| Cash bucket | Best use | Yield profile | Liquidity | Tax treatment | Protection | Accessibility |

|---|---|---|---|---|---|---|

| Treasury bills | Tax-aware cash, 1–12 month ladders | 4-week T-bill coupon equivalent: 3.69% on 05/29/2026 | Matures on schedule; sellable before maturity | Federal taxable; exempt from state and local income tax | Backed by U.S. government | TreasuryDirect or brokerage |

| High-yield savings accounts | Emergency fund and daily-access cash | Top accounts near 5.00% APY, often capped or conditional | Very high | Federal, state, and local taxable | FDIC or NCUA coverage if eligible | Easy for small balances |

| Money market funds | Brokerage cash and settlement cash | Variable 7-day yield tied to short-term rates | Generally same-day or next-day | Tax depends on fund holdings | Not FDIC-insured | Easy inside brokerages |

| Brokered CDs | Known spending date and rate lock | Fixed rate at purchase | Lower if sold before maturity | Federal, state, and local taxable | FDIC coverage if issued by insured bank and within limits | Strong for larger ladders |

The under-discussed lever is taxes. A 3.75% Treasury bill can beat a 4.00% taxable savings account for a saver in a state with income tax, because T-bill interest is exempt from state and local income taxes.

For a saver facing a 5% state income tax rate, a 3.75% T-bill has a rough state-tax-adjusted equivalent of about 3.95%. At a 9% state tax rate, the rough equivalent rises to about 4.12%. That does not eliminate federal taxes, but it changes the comparison.

T-Bills: Best When Taxes Matter

Treasury bills are the cleanest cash instrument for investors who want a defined maturity and U.S. government backing. On 05/29/2026, the Treasury listed coupon-equivalent yields of 3.69% for 4-week bills, 3.68% for 13-week bills, 3.75% for 26-week bills, and 3.79% for 52-week bills.

That shape rewards investors who can ladder cash instead of keeping everything overnight. A simple ladder can hold money across 4-week, 13-week, and 26-week bills so part of the balance matures regularly.

The drawback is access. A T-bill held to maturity is simple. A T-bill sold before maturity can move with market rates, especially if yields shift after purchase. For investors comparing short-term yields with borrowing costs, the same rate mechanics also matter for Treasury yields and mortgage rates.

HYSAs: Best For Emergency Money

High-yield savings accounts are still the easiest place for true emergency cash. The main advantage is operational: money can usually move faster than from a T-bill ladder, and small balances can earn competitive APYs without brokerage complexity.

The risk is headline APY marketing. Some 5.00% APY offers in May 2026 apply only to limited balances, require direct deposit, or drop sharply above a cap. A saver with $5,000 may get the advertised rate. A saver with $75,000 may earn a much lower blended yield.

The protection is stronger than many alternatives when the account is at an FDIC-insured bank or NCUA-insured credit union and stays within coverage limits. The FDIC standard limit is $250,000 per depositor, per insured bank, per ownership category. That makes HYSAs useful for emergency reserves, tax reserves, and near-term expenses.

Readers who want product-level comparisons can use this pillar with a dedicated high-yield savings account guide.

Money Market Funds: Best For Brokerage Cash

Money market funds are most useful when cash already sits inside a brokerage account. They typically invest in short-term instruments such as Treasury bills, government securities, repurchase agreements, certificates of deposit, commercial paper, or municipal securities, depending on the fund type.

The key distinction is protection. A money market fund is not a bank deposit. It is not FDIC-insured. Most retail and government money market funds seek to maintain a stable $1.00 net asset value, but the SEC still warns that funds can lose value in stress scenarios.

This does not make money market funds unsuitable. It makes fund selection important. Government and Treasury money market funds are usually the most conservative. Prime funds may offer slightly higher yields but can carry more credit and liquidity complexity.

For taxable investors, Treasury-only money market funds may also pass through some state-tax-exempt income, depending on holdings and state rules. That can make them a practical bridge between T-bills and brokerage convenience.

Brokered CDs: Best For Known Spending Dates

Brokered CDs make sense when the goal is to lock a known rate for a known date. They can be especially useful for larger balances because investors can buy CDs from multiple issuing banks through one brokerage and spread exposure across FDIC limits.

The trade-off is liquidity. A bank CD often has an early-withdrawal penalty. A brokered CD is usually sold in a secondary market if cash is needed before maturity. That avoids a traditional withdrawal penalty, but it introduces price risk. If rates rise after purchase, the CD may sell below par.

Callable CDs add another layer. If rates fall, the issuer may redeem the CD before maturity, leaving the investor to reinvest at lower rates. The higher headline yield may be compensation for that call risk, not a free premium.

Brokered CDs are strongest when the investor knows the date, checks the issuing bank, stays within insurance limits, avoids confusing call features, and plans to hold to maturity. Cash that might be needed suddenly belongs in a HYSA or very short T-bill ladder instead. Borrowers weighing debt payoff against cash yield should compare after-tax savings returns with actual loan costs, not headline APY; that is where a personal loan rate comparison can be useful.

The Practical Split

The best cash setup in 2026 is usually a mix, not a single account. Emergency cash belongs in a high-yield savings account. Tax-aware cash that can wait one to twelve months fits Treasury bills. Brokerage cash can sit in a government money market fund. Known-date cash can use brokered CDs if liquidity risk is acceptable.

The decision rule is simple: match the instrument to the job. Yield matters, but after-tax yield, access speed, and protection matter more. If the Fed keeps short-term rates near the 3.50% to 3.75% range into summer 2026, cash will remain productive. If rate-cut expectations return, today’s fixed-rate CDs and T-bills may look more valuable. If inflation pressure forces rates higher again, flexible HYSAs and short ladders will adjust faster.

FAQ

What is the safest place to park cash in 2026? For bank cash, an FDIC-insured HYSA within coverage limits is the simplest option. For government-backed cash, Treasury bills offer direct U.S. government backing but are not FDIC-insured bank deposits.

Are T-bills better than high-yield savings accounts? T-bills can be better for taxable investors in states with income tax because Treasury interest is exempt from state and local income taxes. HYSAs are better for immediate access and emergency funds.

Are money market funds FDIC-insured? No. Money market funds are mutual funds, not bank deposits. They can be useful for brokerage cash, but investors should understand fund type, holdings, expense ratio, and liquidity rules.

When should I use brokered CDs instead of T-bills? Brokered CDs work best when you want a fixed rate for a known date and can hold to maturity. T-bills are usually cleaner when state tax treatment, simplicity, and Treasury backing are the priority.

Sources and Further Reading

- Daily Treasury Bill Rates — U.S. Department of the Treasury — 05/29/2026 — https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?field_tdr_date_value=2026&type=daily_treasury_bill_rates ([U.S. Department of the Treasury][1])

- Interest Income Reporting for Marketable Treasury Securities — TreasuryDirect / Bureau of the Fiscal Service — 05/30/2026 — https://www.treasurydirect.gov/forms/sec0011.pdf ([TreasuryDirect][2])

- Understanding Deposit Insurance — FDIC — 04/01/2024 — https://www.fdic.gov/resources/deposit-insurance/understanding-deposit-insurance ([FDIC][3])

- Money Market Funds: Investor Bulletin — Investor.gov / SEC — 11/04/2024 — https://www.investor.gov/introduction-investing/general-resources/news-alerts/alerts-bulletins/investor-bulletins/updated-12 ([Investor][4])

- Your Cash Could Be Earning More—Here's Where to Find Today's Top Rates — Investopedia — 05/30/2026 — https://www.investopedia.com/your-cash-could-be-earning-more-here-s-where-to-find-today-s-top-rates-11987302 ([Investopedia][5])