If you are shopping for a home this month, the link between the jobs report and mortgage rates deserves your attention. On June 5, 2026, the Bureau of Labor Statistics releases the May payrolls report at 8:30 a.m. ET — and the number could nudge your borrowing costs within hours. This guide explains how a single labor-market data point travels from a government press release to the rate a lender quotes you, and what a strong or weak report would mean for locking your rate in June 2026.

How the Jobs Report Reaches Mortgage Rates

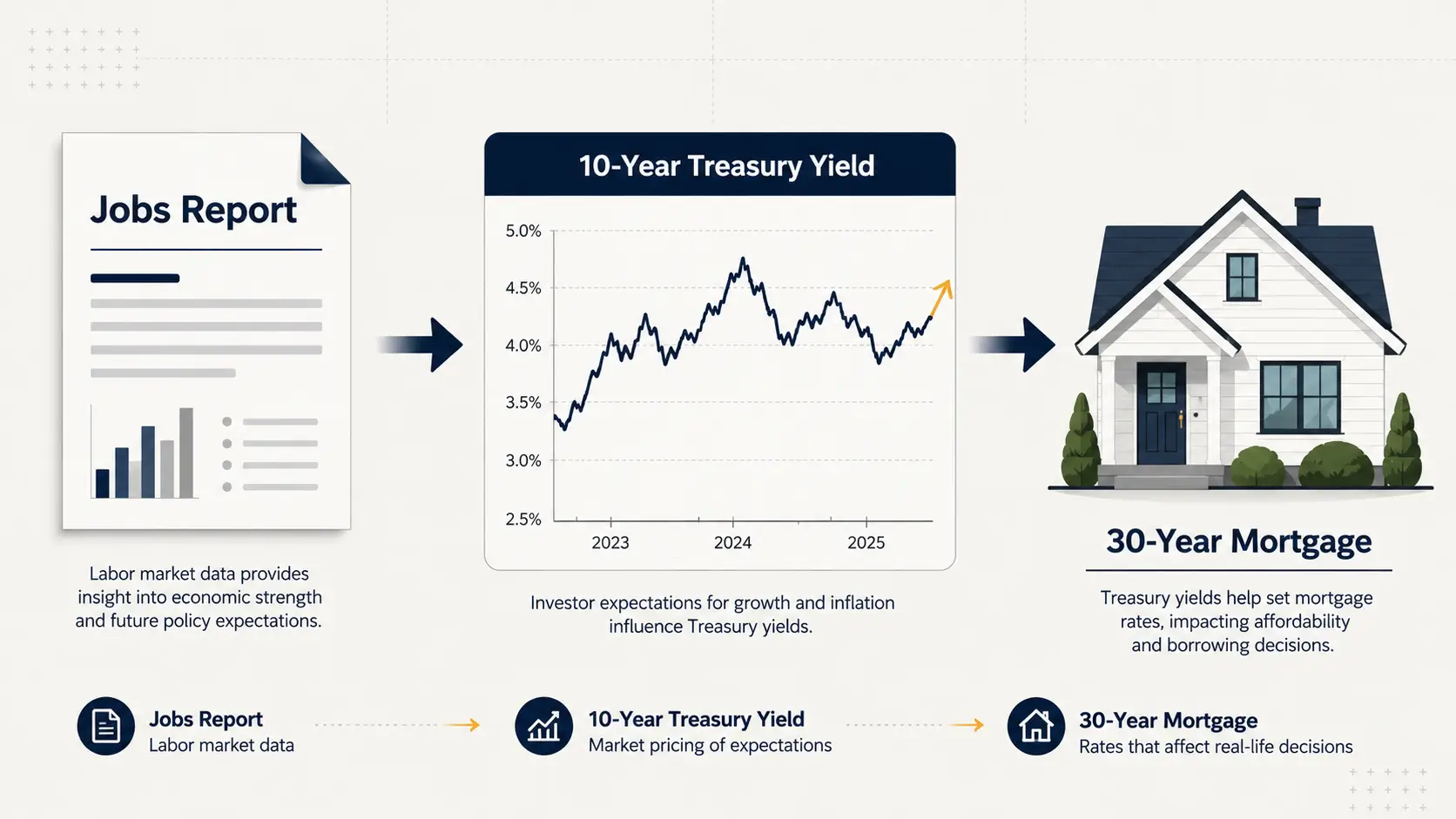

Mortgage rates do not move on the Federal Reserve's say-so. The 30-year fixed rate tracks the 10-year Treasury yield, plus a premium that lenders and investors add on top. When the jobs report lands, bond traders reprice how fast the economy is growing and what the Fed is likely to do next. That repricing shows up first in Treasury yields, then in the rate sheets lenders publish the same morning.

The direction is usually straightforward. A stronger-than-expected payrolls number signals a hotter economy, which pushes yields — and mortgage rates — up. A weaker number does the opposite. The 10-year Treasury's pull on mortgage rates is the single most important relationship for a buyer to understand.

That premium matters too. As of June 2, 2026, the 10-year Treasury yielded 4.46% while the average 30-year fixed mortgage sat near 6.54%. That gap of roughly two percentage points is wider than the historical norm of about 1.7 points — a reminder that even if yields fall, mortgage rates may not drop as much as buyers expect.

Where Things Stand Before the June 5 Report

April's report, released May 8, 2026, showed nonfarm payrolls rising 115,000 — nearly double the consensus forecast near 62,000. The unemployment rate held at 4.3%, and March was revised up to 185,000 job gains. It marked the first back-to-back monthly increase in nearly a year, pointing to a labor market that is cooling slowly rather than cracking.

The complication is inflation. The April Consumer Price Index, released May 12, 2026, showed prices up 3.8% from a year earlier — the hottest reading since May 2023, pushed higher in part by oil prices tied to the U.S. conflict with Iran. As a result, bond markets have shifted from expecting rate cuts to pricing a real chance of a Fed rate hike before year-end. That backdrop changes how the jobs report will land.

A Hot Print vs. a Soft Print: What Each Means for Your Rate Lock

For most of the past two years, the playbook was simple: a weak jobs report meant lower mortgage rates were coming. In June 2026, that reflex is unreliable.

If the May report runs hot — payrolls well above forecast, unemployment below 4.3%, or average hourly earnings accelerating — expect the 10-year yield to climb and mortgage rates to follow within a day. Wage growth is the figure to watch most closely, because hot earnings revive inflation fears and can lift rates even when the headline job count looks modest. A buyer near a decision point would have reason to lock before the release.

If the report comes in soft, the usual relief may be muted. With inflation running at 3.8%, a weak payrolls number competes with the bond market's inflation anxiety. Yields could ease, but a durable drop in mortgage rates would likely require cooler inflation data too — not just one cool jobs print.

The Risk Buyers Underestimate

The biggest mistake is treating the jobs report as a one-way ticket to lower rates. Today's market is driven as much by inflation and geopolitics as by the labor market. Oil prices, the path of the Iran conflict, and the next CPI release all sit alongside payrolls as rate drivers.

There is also the spread. The same forces that pushed mortgage rates near 7% earlier in 2026 can widen the cushion between Treasury yields and mortgage rates during volatile periods, blunting the benefit of any yield decline. Buyers waiting for a single data point to deliver a clean rate drop may wait a long time.

The Takeaway for June 2026 Buyers

The jobs report still moves mortgage rates — but in June 2026 it does so through an inflation-tinted lens. The payrolls-to-yields-to-mortgage chain is intact; what has changed is that good news for the labor market is now bad news for rates, and bad news no longer guarantees relief.

The practical takeaway: if you are close to closing and the quoted rate works for your budget, the June 5 report is a coin flip you may not want to gamble on — locking removes the risk. If you have more time, watch the May CPI release that follows, because inflation, not jobs alone, will set the direction of mortgage rates through the summer.

Is the jobs report the same as nonfarm payrolls? The monthly Employment Situation report includes nonfarm payrolls, the unemployment rate, and average hourly earnings. Markets often use "jobs report" and "payrolls" interchangeably, but rate movements depend on all three figures together.

How fast do mortgage rates react to the jobs report? Treasury yields can move within minutes of the 8:30 a.m. ET release, and many lenders adjust their rate sheets the same morning. The effect on quoted mortgage rates is often visible by midday.

Should I lock my mortgage rate before the June 5, 2026 report? If you are close to closing and the quoted rate fits your budget, locking removes the risk of an adverse move, since the report could push rates in either direction. This is general information, not personalized financial advice.

Why might weak jobs data fail to lower mortgage rates in 2026? With inflation at 3.8% as of April 2026, bond markets are focused on price pressures. A soft jobs print may not rally bonds enough to pull mortgage rates down without cooler inflation data alongside it.

Sources and Further Reading

- Employment Situation — April 2026 — U.S. Bureau of Labor Statistics — 05/08/2026 — https://www.bls.gov/news.release/archives/empsit_05082026.htm

- Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity (DGS10) — FRED, Federal Reserve Bank of St. Louis — 06/02/2026 — https://fred.stlouisfed.org/series/DGS10

- Current Mortgage Rates — Bankrate — 06/02/2026 — https://www.bankrate.com/mortgages/mortgage-rates/

- Today's Mortgage Rates: June 2, 2026 — U.S. News & World Report — 06/02/2026 — https://money.usnews.com/loans/mortgages/articles/mortgage-rates-today-june-2-2026

- United States Non Farm Payrolls — Trading Economics — 06/01/2026 — https://tradingeconomics.com/united-states/non-farm-payrolls