Many households still feel squeezed because the pressure has shifted from prices to payments.

This guide explains how high interest rates affect household budgets in 2026, why borrowing costs remain difficult to escape, and which expenses deserve the closest attention before taking on new debt.

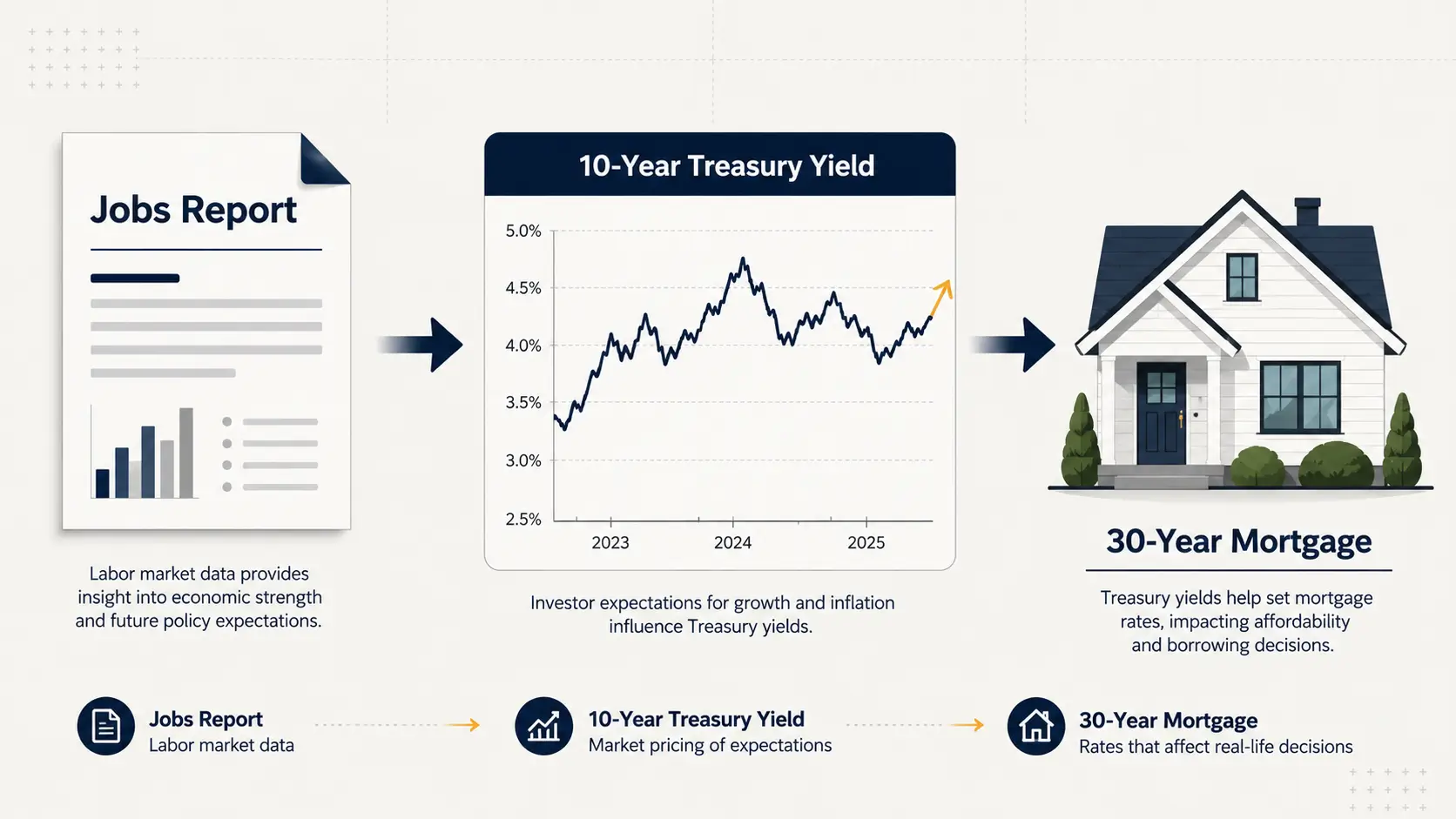

As of 04/29/2026, the Federal Reserve held the federal funds target range at 3.50% to 3.75%. As of 05/14/2026, the average 30-year fixed mortgage rate was 6.36%. Total U.S. household debt reached $18.8 trillion, or eighteen point eight trillion dollars, in Q1 2026, according to the New York Fed.

The practical takeaway is simple: when rates stay high, monthly payments absorb more income before households can save, invest, or spend freely.

Why Interest Rates Still Matter After Inflation Slows

Inflation and interest rates are related, but they are not the same household problem.

Inflation measures how fast prices rise. Interest rates determine how expensive debt becomes. A household may see slower price growth but still face expensive credit card balances, auto loans, and mortgages.

That distinction matters again in 2026. The Consumer Price Index rose 3.8% for the 12 months ending April 2026, up from 3.3% in March. Core inflation, excluding food and energy, rose 2.8% over the same period.

For household budgets, that keeps the pressure two-sided. Everyday costs are still rising, while financing costs remain high enough to make large purchases harder to absorb.

Where High Rates Hit Monthly Budgets First

High interest rates usually hit budgets through required payments, not through one dramatic shock.

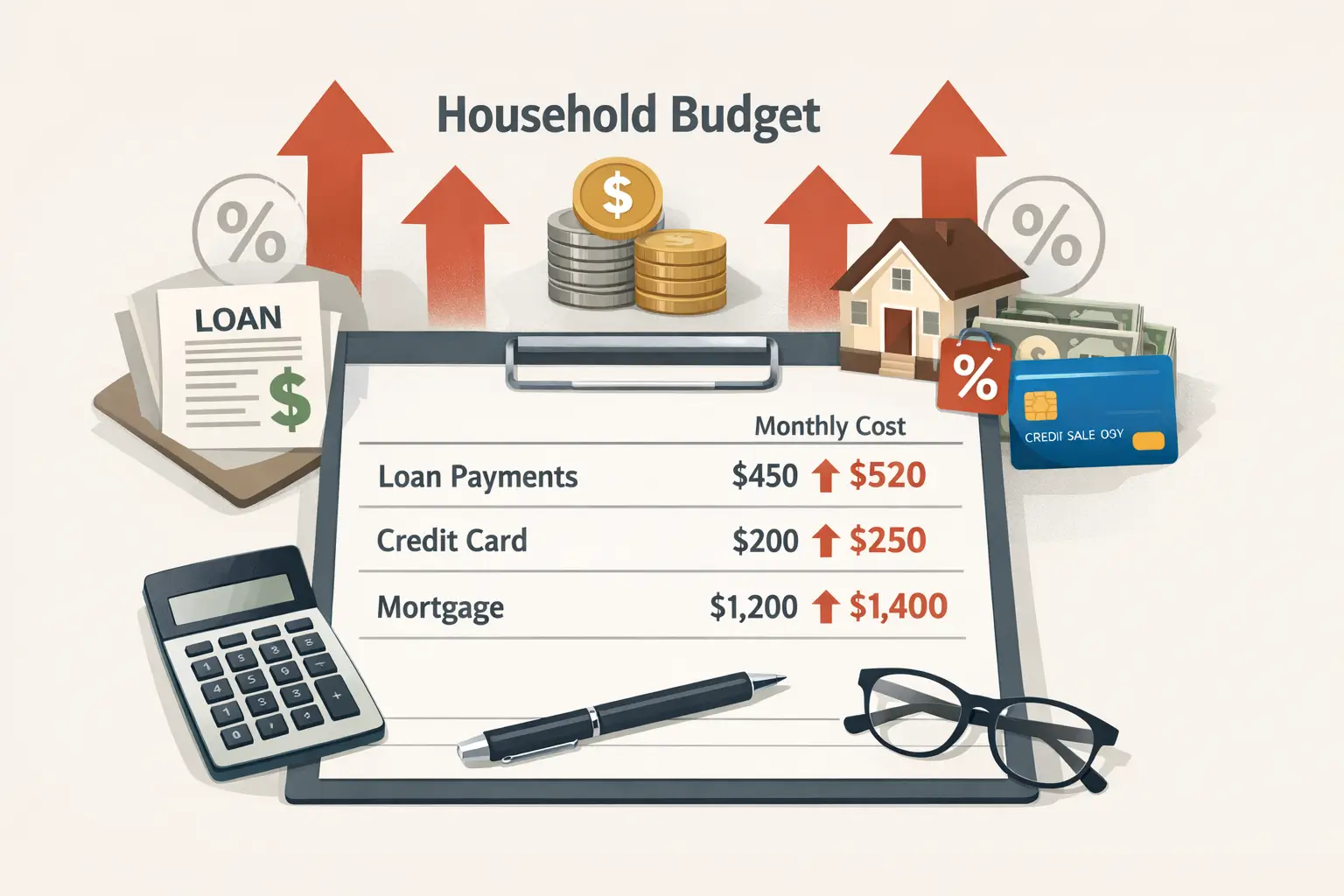

Credit cards feel it first. In the Fed’s March 2026 consumer credit release, credit card plans carried an average APR of 21.00% across all accounts in Q1 2026, while accounts assessed interest averaged 21.52%. That makes revolving balances one of the most expensive forms of household debt. For more context, see why credit card debt keeps growing in 2026.

Auto loans are another pressure point. New York Fed data showed auto loan balances increased by $18 billion in Q1 2026 to $1.69 trillion, or one point sixty-nine trillion dollars. When rates are high, even a modest vehicle purchase can become a large fixed monthly obligation.

Housing is the largest constraint for many families. A 6.36% 30-year mortgage rate does not only raise payments. It also reduces purchasing power, limits refinancing options, and keeps many homeowners locked into older mortgages they do not want to give up.

Who Feels the Impact First

High rates do not affect every household equally.

Lower-income households usually feel the pressure first because they have less cash available after rent, groceries, insurance, and transportation. When borrowing costs rise, there is less room to absorb a surprise bill.

Younger households also face more direct exposure. Many are buying their first homes, financing vehicles, or carrying newer debt at today’s rates rather than older, cheaper rates.

Borrowers with revolving or variable-rate debt face the fastest adjustment. Credit card balances, some personal loans, and adjustable-rate products can become more expensive before wages or savings catch up.

That is why high rates often show up first in credit stress, delayed purchases, and reduced discretionary spending.

Why This Matters Again Now

The current risk is that rate relief may arrive later than households expect.

The Fed’s 04/29/2026 statement kept rates unchanged and said future adjustments would depend on incoming data, inflation pressures, and the balance of risks. That keeps the timeline for easier borrowing costs uncertain, especially after April CPI accelerated to 3.8%.

For households, that means budgets should be built around current rates, not hoped-for cuts. A payment that only works if rates fall soon is not a safe payment.

For investors and readers tracking the broader economy, household budgets are an early signal. If credit card stress, auto delinquencies, or weak refinancing activity worsen, consumer spending can slow before headline economic data fully reflects the strain. That is also why rate-cut expectations remain important for personal finance decisions.

Practical Budget Moves in a High-Rate Period

Households cannot control Fed policy, but they can control exposure to expensive debt.

The first priority is usually high-interest debt. Reducing a credit card balance at a 21% APR often produces more immediate budget relief than chasing small savings elsewhere.

The second priority is avoiding new fixed obligations that leave no margin for error. Before taking on a car loan or mortgage, households should stress-test the payment against one income disruption, one insurance increase, or one unexpected repair.

The third priority is timing. Delaying a financed purchase can be rational when the monthly payment is stretched. Waiting does not guarantee a lower rate, but it can preserve cash and reduce the risk of locking in a payment that limits future flexibility.

What to Watch Next

The next major inflation release is scheduled for 06/10/2026. If inflation remains above the Fed’s 2% goal, borrowing costs may stay restrictive for longer.

Households should also watch mortgage rates, credit card APRs, auto loan delinquencies, and refinancing activity. These indicators show whether payment pressure is easing or spreading.

High interest rates change household budgets gradually. The first effect is a higher payment. The second is less flexibility. The third is a delayed purchase, smaller emergency fund, or slower savings plan.

The forward-looking risk is clear: if inflation stays sticky and debt keeps rising, even future rate cuts may not fully repair household budgets already stretched by expensive payments.

FAQ

Why do household budgets feel tight even when inflation is lower than its 2022 peak? Because borrowing costs remain high. Credit cards, auto loans, and mortgages can keep monthly payments elevated even when price inflation slows.

Which household expenses are most affected by high interest rates? Credit card payments, auto loans, and mortgage costs are usually affected first because they depend directly on borrowing rates.

Who is most vulnerable to high interest rates? Lower-income households, younger borrowers, first-time homebuyers, and people with revolving or variable-rate debt usually feel the pressure earliest.

Should households wait for rate cuts before making big purchases? Not always. But a purchase should make sense at current rates. Relying on future rate cuts to make a payment affordable adds financial risk.

Sources and Further Reading

- Federal Reserve Issues FOMC Statement — Federal Reserve — 04/29/2026 — https://www.federalreserve.gov/newsevents/pressreleases/monetary20260429a.htm

- Mortgage Rates — Freddie Mac — 05/14/2026 — https://www.freddiemac.com/pmms

- Household Debt Balances Rise Slightly as Delinquency Transition Rates Hold Steady — Federal Reserve Bank of New York — 05/12/2026 — https://www.newyorkfed.org/newsevents/news/research/2026/20260512

- Consumer Price Index Summary — Bureau of Labor Statistics — 05/12/2026 — https://www.bls.gov/news.release/cpi.nr0.htm

- Consumer Credit - G.19 — Federal Reserve — 05/07/2026 — https://www.federalreserve.gov/releases/g19/current/