The soft landing survives another test, but the Federal Reserve gets no clean escape route. The initial jobless claims May 2026 report shows layoffs remain contained, while the Chicago Business Barometer rebounded sharply on May 29. Yet more workers are remaining on benefits and April inflation accelerated, leaving the economy resilient without making interest-rate relief easier.

The clean takeaway is not that labor weakness disappeared. It is that business activity strengthened before slower reemployment became a broader downturn signal.

Initial Jobless Claims May 2026 Show Hiring Friction

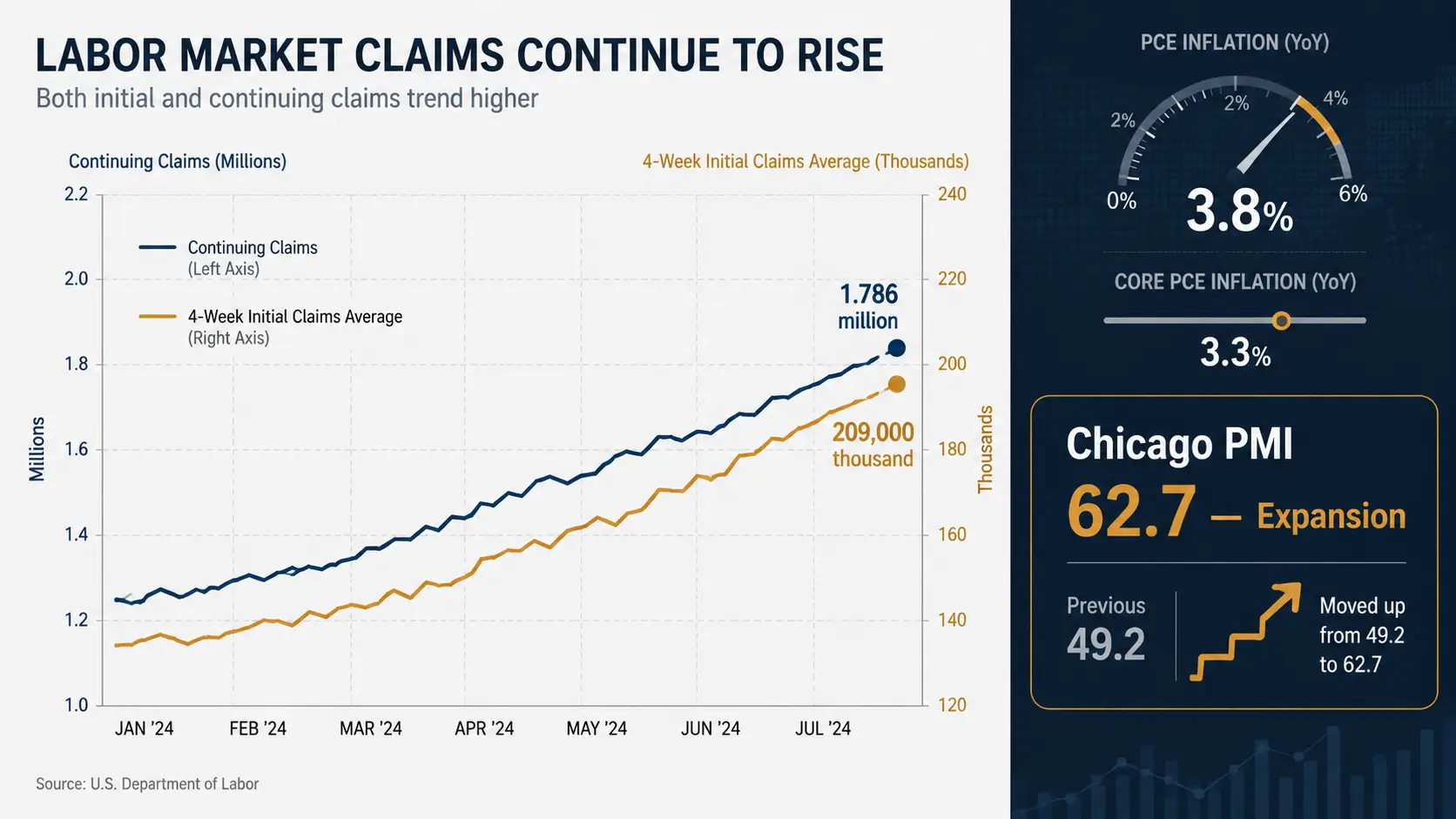

The chart that matters still compares new job losses with workers remaining unemployed. For the week ended May 23, initial claims rose to 215,000, up 5,000 from the revised prior week. The four-week moving average increased to 209,000, up 6,250, in the Labor Department release dated May 28.

Those readings do not show widespread layoffs. Initial claims remained below the 236,000 level reported for the comparable week in 2025.

The less comfortable signal is continuing claims. For the week ended May 16, insured unemployment increased to 1.786 million, up 15,000 from the revised prior week. Its four-week moving average rose to 1.773 million.

Single takeaway: companies are not broadly cutting jobs, but unemployed workers may be taking longer to find their next position. That distinction matters when restrictive borrowing costs are already influencing business hiring decisions.

Chicago PMI Clears the Growth Test — for Now

The data point that was missing from the earlier scorecard arrived on May 29. The Chicago Business Barometer climbed 13.5 points to 62.7 in May, up from 49.2 in April, according to ISM Chicago. The reading is the highest since January 2022 and places regional business activity back above the neutral 50 threshold.

The rebound was driven by gains in new orders, production, order backlogs and supplier deliveries. Employment declined, providing a partial counterweight to the headline surge.

Single takeaway: Chicago activity does not confirm an imminent business contraction. But the decline in the employment component supports the same warning visible in continuing claims: stronger activity is not yet translating into a cleaner labor-market picture.

For markets, that limits the value of the PMI relief. Growth-sensitive assets gain support from an expansionary activity reading, but rate-sensitive assets still face the question of whether persistent inflation blocks faster monetary easing.

Why This Matters Again Now

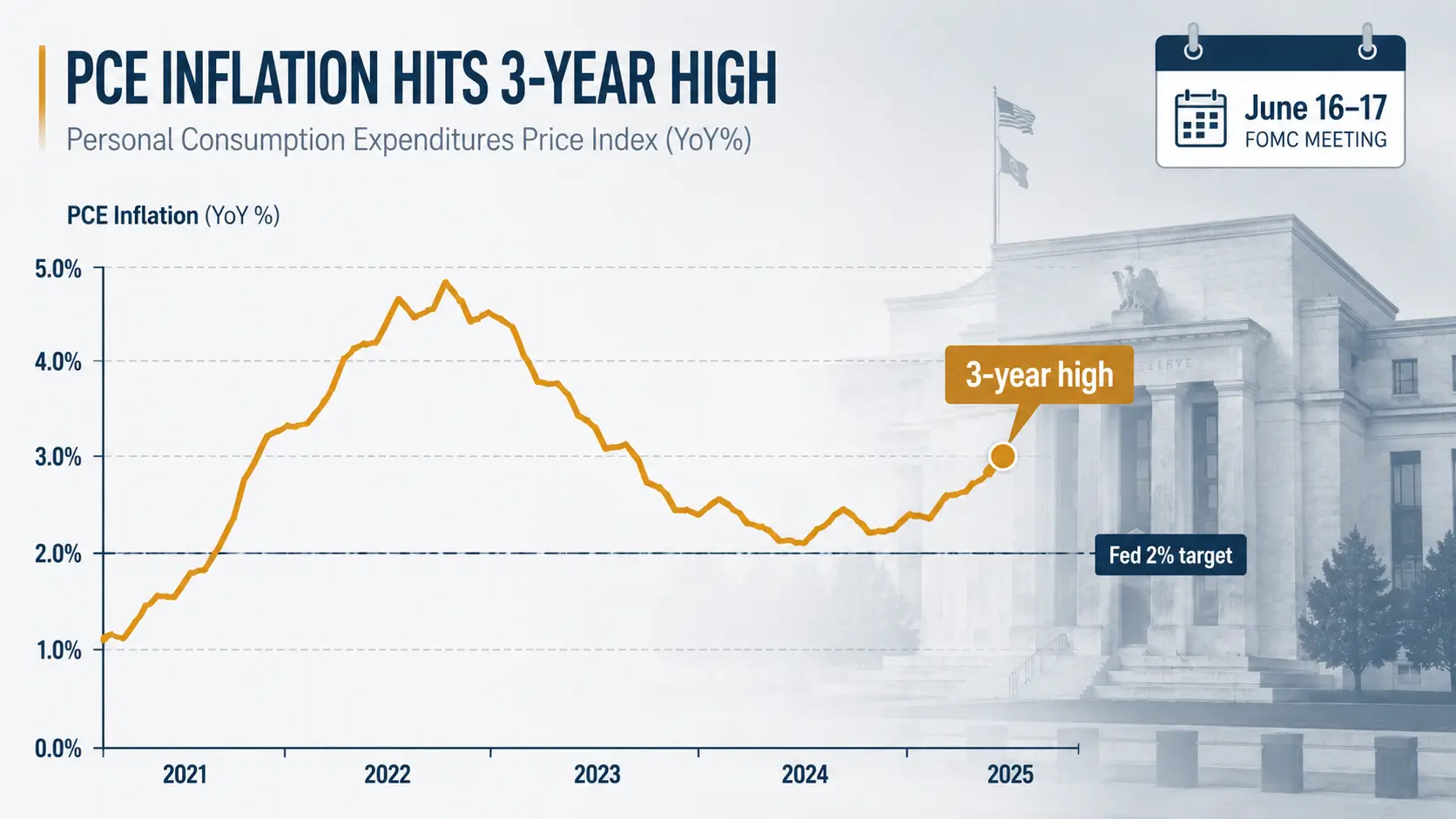

The May 29 PMI rebound arrived one day after inflation and growth data narrowed the margin for a painless landing. In the April report released May 28, the PCE price index rose 3.8% from one year earlier, while core PCE increased 3.3%. Real consumer spending rose only 0.1% in April, and the personal saving rate fell to 2.6%.

Growth is positive but less secure than previously reported. First-quarter real GDP was revised down on May 28 to a 1.6% annualized rate, from the earlier 2.0% estimate.

Single takeaway: the soft landing is still intact, but it now depends on business activity staying firm while consumers absorb higher prices and slower job transitions. That is a difficult policy combination. The Fed sees enough resilience to avoid rushing into cuts, yet enough pressure on households and job seekers to keep downside growth risks alive.

That tension remains central to the 2026 Fed rate-cut investor guide: weaker labor momentum alone does not guarantee faster easing when core inflation remains above the central bank’s objective.

What Investors Should Watch Next

Chicago PMI has moved the narrative from “possible break” to “resilience under pressure.” The expansion signal weakens the immediate recession case, but it does not erase the rise in continuing claims or the inflation constraint.

The next risk is a split economy: activity indicators remain firm enough to delay rate cuts, while households face slower income growth, elevated prices and longer job searches. If continuing claims keep climbing while inflation remains sticky, the soft landing will look less like a clean resolution and more like a narrow path markets must continuously reprice.

FAQ

What did the initial jobless claims May 2026 report show? Initial claims rose to 215,000 for the week ended May 23, 2026, while the four-week moving average increased to 209,000. The report still indicates contained layoffs rather than a broad labor-market break.

Why are continuing claims important for the soft-landing outlook? Continuing claims increased to 1.786 million for the week ended May 16, 2026. That suggests some workers may be taking longer to find new jobs even while new layoffs remain limited.

What was the Chicago PMI reading for May 2026? The Chicago Business Barometer rose to 62.7 in May 2026 from 49.2 in April, returning to expansion territory and reaching its highest level since January 2022.

Does the new data mean the Fed can cut interest rates soon? Not necessarily. Business activity improved, but April core PCE inflation still rose 3.3% year over year, limiting the Fed’s ability to respond quickly to softer labor signals.

Sources and Further Reading

- Unemployment Insurance Weekly Claims — U.S. Department of Labor — 05/28/2026 — https://www.dol.gov/ui/data.pdf

- Chicago Business Barometer™ & Research — ISM Chicago — 05/29/2026 — https://chicago.ismworld.org/news-publications/reports/research-survey/

- Key US Inflation Measure Posts Largest Annual Increase in Three Years — Reuters — 05/28/2026 — https://www.reuters.com/business/us-pce-inflation-firmer-april-2026-05-28/