The best high yield savings accounts 2026 still pay meaningful interest on cash, but the headline rate needs scrutiny. Among the accounts reviewed here, Varo displays a 5.00% annual percentage yield, or APY, only on balances up to $5,000 (five thousand dollars) after monthly qualification rules are met. Other leading options trade a lower headline APY for easier access, fewer conditions or broader deposit coverage. ([Varo Bank][1])

This comparison focuses on five questions that matter for emergency funds and short-term cash: the APY available, the balance or activity requirement, the deposit-insurance structure, how quickly money can be moved, and whether ATM access is built in. Rates were reviewed on 05/29/2026; each provider sets variable APYs and may change them before or after an account is opened.

The Best High Yield Savings Accounts 2026, Compared

| Account | APY displayed by provider | Minimums or conditions | Deposit-protection structure | Transfer and ATM access | Best fit |

|---|---|---|---|---|---|

| Varo Savings Account | 5.00% on up to $5,000; 2.50% above that balance | No minimum balance; receive at least $1,000 (one thousand dollars) in qualifying direct deposits monthly and end the month with positive Varo balances | Varo Bank, N.A., Member FDIC | Savings requires a Varo Bank Account; debit-card ATM access through Varo banking setup | Smaller qualifying emergency funds |

| SoFi Checking and Savings | Up to 3.80% promotional APY for eligible new members | Promotion requires eligible direct deposit or qualifying deposits; conditions apply | SoFi Bank, N.A., Member FDIC | Integrated checking and debit-card access; Allpoint ATM network | Readers wanting spending and saving in one platform |

| CIT Bank Platinum Savings | 3.75% on balances of $5,000 or more; 0.25% below $5,000 | $100 (one hundred dollars) minimum opening deposit; higher tier requires at least $5,000 | FDIC-insured CIT Bank deposit account | Online and mobile transfers; ATM access available through linked CIT banking services | Savers consistently holding at least $5,000 |

| Marcus Online Savings Account | 3.50% APY | No minimum deposit; no account fee | Goldman Sachs Bank USA, Member FDIC | Same-day transfers of $100,000 (one hundred thousand dollars) or less under stated timing rules; no debit or ATM card | Simplicity and scheduled transfers |

| Wealthfront Cash Account | 3.30% base APY; up to 4.20% with stacked eligible boosts | No account fee; higher promotional yield depends on client and activity requirements | Cash sweep through program banks; up to $8 million (eight million dollars) in FDIC insurance through program banks | Free instant withdrawals to eligible accounts; 19,000-plus fee-free ATMs | Larger cash balances and fast digital access |

Varo is the only reviewed option publishing a 5.00% APY tier, but the limit matters: the premium rate covers only the first $5,000. SoFi, CIT, Marcus and Wealthfront publish lower or conditional yields, but may be better matches for balances beyond Varo’s cap or for readers who prioritize access over the highest advertised number. ([Varo Bank][1])

Our Picks: Rate, Access and Trade-Offs

Varo Savings Account: Best for earning 5.00% on a smaller balance

Varo publishes the highest APY in this comparison: 5.00% on balances up to $5,000 once the customer qualifies. The account starts at 2.50% APY, and the premium rate requires at least $1,000 in qualifying direct deposits during the month plus positive balances across Varo accounts at month-end. Its disclosure states that the APY information is accurate as of 01/30/2026. ([Varo Bank][1])

Pros: The 5.00% APY can be useful for the first layer of an emergency fund, particularly for a paycheck depositor who already meets the activity rule. Varo is a chartered bank and Member FDIC.

Cons: A saver with more than $5,000 should not apply the headline APY to the entire balance. Cash above the cap receives 2.50% APY under the published terms, reducing the blended yield.

Decision point: Varo is compelling for a qualified $5,000 cash reserve. It becomes less attractive as a standalone home for a substantially larger emergency fund.

SoFi Checking and Savings: Best for integrated cash management

SoFi advertises up to 3.80% APY for eligible new Checking and Savings members through a limited-time boost, with the displayed promotional rate current as of 05/28/2026. Qualification requires an eligible direct deposit or qualifying deposits under the promotion terms, and maintaining the required activity is necessary to continue receiving the boost for its stated period. ([SoFi][2])

Pros: SoFi combines savings, checking and debit-card access in one relationship. Its banking page also identifies SoFi Bank, N.A. as Member FDIC, while its ATM disclosures provide access to more than 55,000 Allpoint ATMs without a SoFi in-network ATM fee.

Cons: The most appealing APY is promotional and conditional. Readers should review the rate sheet and promotion end date rather than assuming today’s displayed boosted yield will remain available for an entire savings horizon.

Decision point: SoFi fits readers who want cash to earn interest while remaining closely connected to bill payments, debit-card spending and ATM withdrawals.

CIT Bank Platinum Savings: Best for balances above $5,000

CIT Bank Platinum Savings publishes 3.75% APY for balances of $5,000 or more, compared with 0.25% APY below that threshold, with the provider’s APY disclosure dated 01/09/2026. The account requires a $100 opening deposit and carries no monthly service fee under CIT’s published terms. ([Citigroup][3])

Pros: The higher APY applies across the qualifying balance tier rather than only a limited opening slice. That can make CIT easier to evaluate for a saver maintaining more than $5,000.

Cons: Falling below the balance threshold sharply reduces the published APY. That structure is poorly suited to an emergency fund likely to be drawn down below $5,000.

Decision point: CIT is a cleaner rate proposition for a stable cash reserve above the threshold, but not for an account frequently used for withdrawals.

Marcus Online Savings: Best for simple transfers without account conditions

Marcus publishes a 3.50% APY for its Online Savings Account as of 05/29/2026, with no fees and no minimum deposit. The account is offered by Goldman Sachs Bank USA and is FDIC-insured within applicable ownership limits. Marcus also states that transfers of $100,000 or less requested through Marcus by 12 p.m. ET on a business day are processed by 5 p.m. ET that day, subject to transfer conditions. ([Marcus][4])

Pros: The account avoids activity-based APY qualifications and offers a clearly stated transfer process. That simplicity matters for savers who want an emergency reserve separate from everyday spending.

Cons: Marcus savings accounts do not offer a debit card or ATM card. Cash must generally be transferred to an external bank or withdrawn by other supported methods before it can be spent.

Decision point: Marcus suits readers who value a straightforward savings account and can tolerate one additional step before spending the money.

Wealthfront Cash Account: Best for large balances and digital access

Wealthfront is not a bank savings account; its Cash Account uses program banks. The product page publishes a 3.30% base APY as of 01/30/2026 and advertises up to 4.20% APY when eligible boosts are combined. New clients can receive a temporary 0.65 percentage-point boost for three months on up to $150,000 (one hundred fifty thousand dollars), while an additional 0.25 percentage-point increase requires qualifying direct deposit activity and a funded investing account. ([Wealthfront][5])

Pros: Wealthfront publishes up to $8 million in FDIC insurance through program banks, free instant withdrawals to eligible accounts and access to more than 19,000 fee-free ATMs. Those features can matter more than a small APY difference for readers managing larger short-term balances.

Cons: The highest displayed yield is not the permanent base rate. It depends on eligibility requirements and, for part of the boost, a temporary promotional window. Because Wealthfront uses a program-bank structure, readers should review sweep disclosures before relying on expanded deposit coverage.

Decision point: Wealthfront is best evaluated as a cash-management account with broad access features, not as a direct substitute for a single-bank HYSA.

How to Choose the Right Account for Your Cash

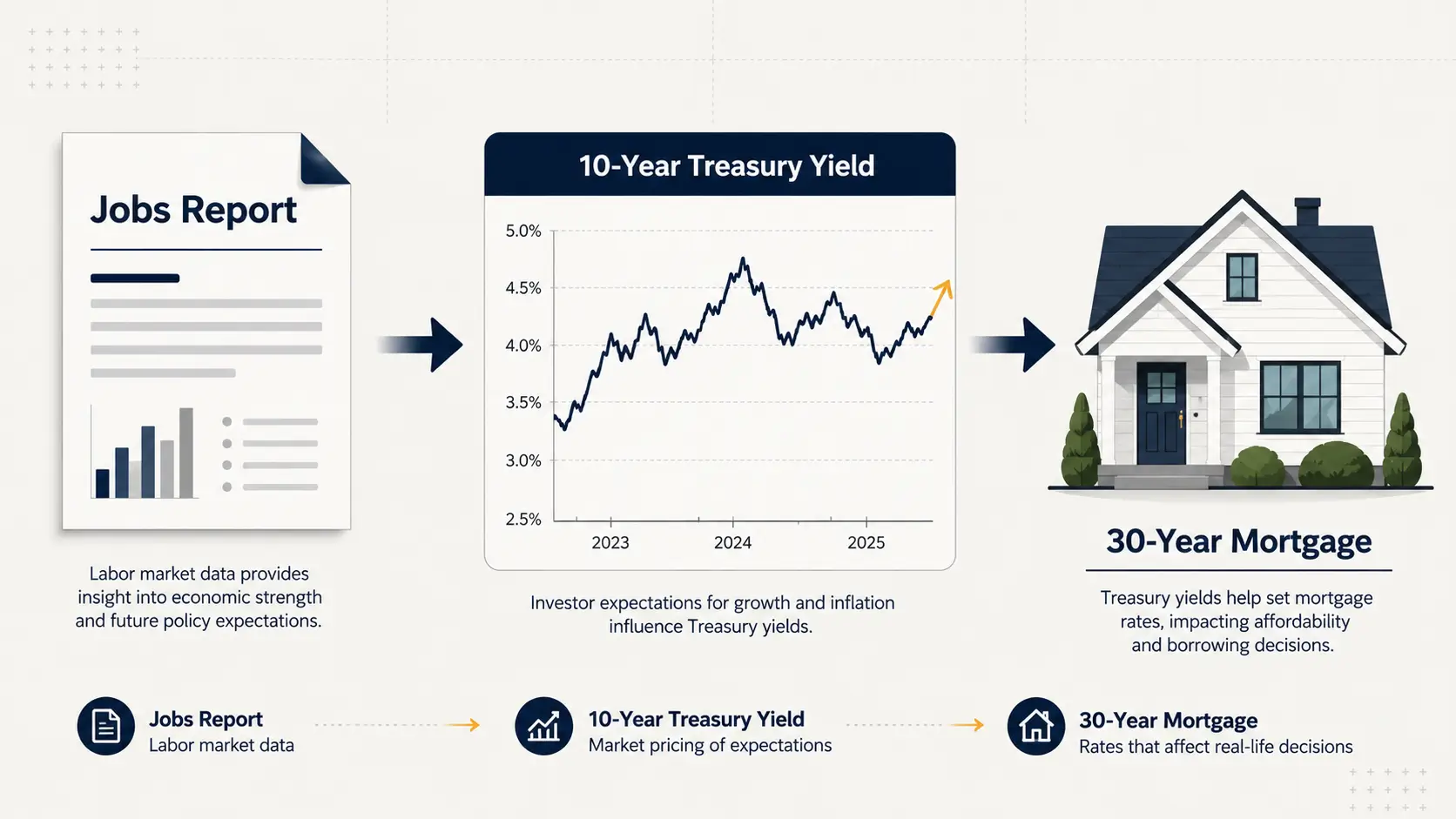

The correct account depends on what the cash is for. A first-line emergency reserve needs immediate access and stable terms. A home down payment fund may justify separating cash from daily spending while monitoring how the 10-year Treasury yield affects mortgage rates. A larger reserve may place more weight on deposit coverage structure than on capturing the last fraction of an APY point.

Rate comparisons should also be made against the real use of the money. A conditional 5.00% APY on a capped balance can be valuable, but it does not automatically beat a lower-rate account for a saver holding tens of thousands of dollars. Likewise, a slightly lower APY may be worth accepting when the account offers faster withdrawals, simpler rules or better operational access.

Readers carrying costly unsecured debt should compare the guaranteed interest cost of that debt with the variable yield available on cash. Maintaining an emergency reserve remains prudent, but cash held beyond that reserve may deserve comparison with repayment options covered in our personal loans guide for U.S. borrowers.

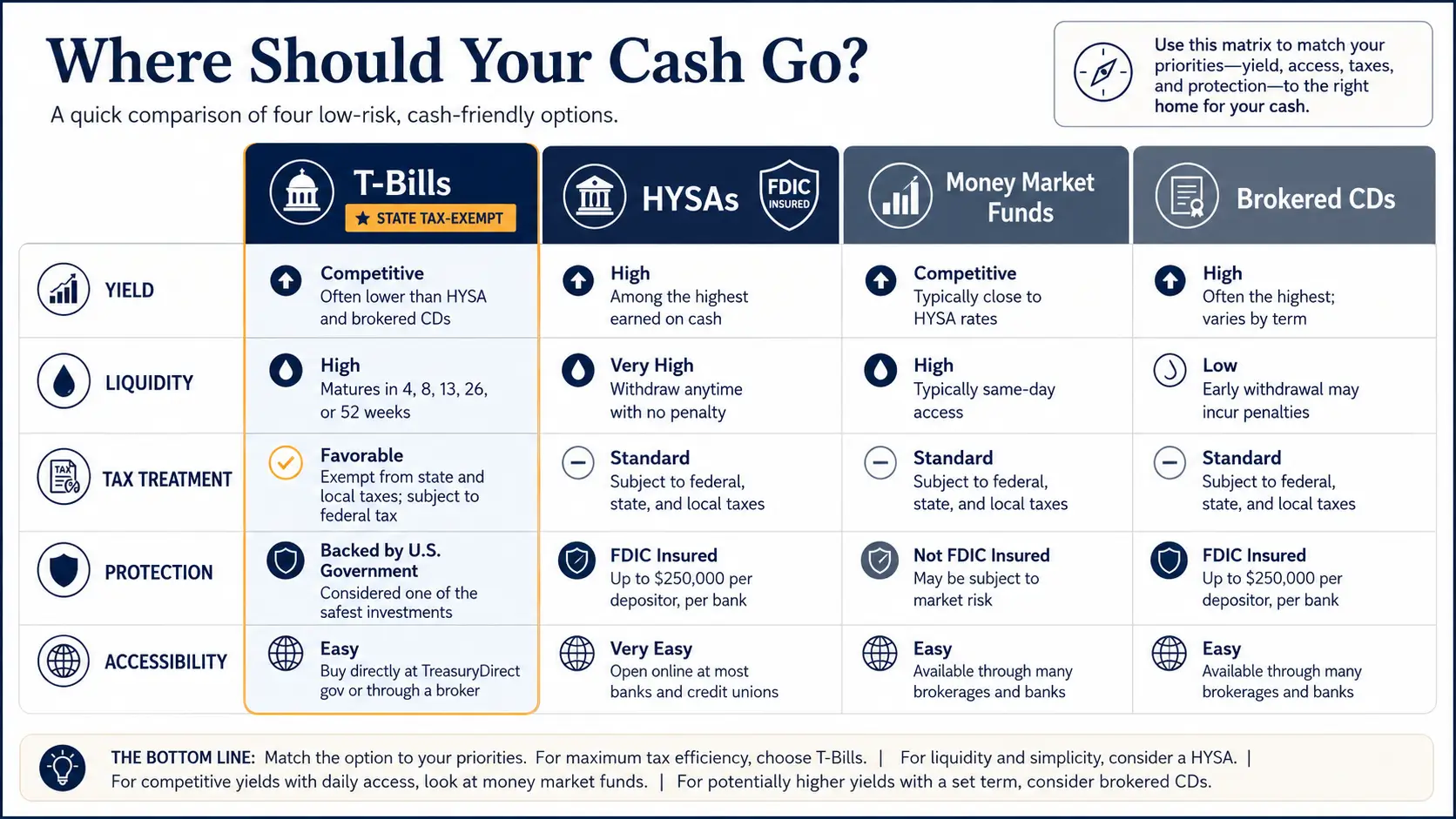

When a Money Market Fund Beats an HYSA

A money market fund can make more sense than an HYSA when the fund’s current after-fee yield is meaningfully above the savings-account APY, the cash is held inside a brokerage relationship, and same-day debit-card or ATM access is not essential.

The comparison must be disciplined. An HYSA is built around bank-deposit access and FDIC coverage within applicable limits or sweep-program terms. A money market fund should be evaluated by its seven-day yield, expense ratio, settlement access, tax treatment and protection structure. For cash that must function as immediate emergency money, convenience and deposit coverage may outweigh a modest yield advantage.

Readers building a broader cash-allocation strategy can continue with our forthcoming money market funds versus high-yield savings guide.

Bottom Line

The best high yield savings accounts 2026 do not offer one universal winner. Varo offers the strongest published headline yield for qualified balances up to $5,000. CIT is more straightforward for savers consistently holding at least that amount. Marcus emphasizes simplicity, SoFi integrates spending and saving, and Wealthfront offers a distinctive cash-management structure for larger balances and digital access.

The practical rule is simple: compare the APY you can actually qualify for on the balance you actually hold, then check transfer access and deposit-protection structure before opening an account. Because every APY in this comparison is variable, the strongest account today may not remain the strongest after the next interest-rate move.

FAQ

What is the highest high-yield savings APY reviewed for 2026? Varo publishes a 5.00% APY tier on balances up to $5,000 after monthly qualification requirements are met. Balances above that cap earn the lower APY stated in Varo’s terms. ([Varo Bank][1])

Is Wealthfront Cash Account a high-yield savings account? No. Wealthfront states that it is not a bank and uses program banks for its Cash Account. It is included here because readers comparing high-yield cash options may value its base APY, withdrawal features and expanded FDIC sweep structure. ([Wealthfront][5])

Are high-yield savings accounts FDIC-insured? Deposit accounts offered directly through FDIC-member banks are insured within applicable FDIC limits and ownership categories. Readers using cash sweep programs should review how and when funds are allocated to participating banks.

Should an emergency fund be kept in the highest-APY account? Not always. Emergency cash should balance yield with fast access, simple qualification rules and reliable deposit protection. A higher advertised APY may be less useful if it is capped, temporary or difficult to maintain.

Sources and Further Reading

- High-Yield Savings Account — Varo Bank — 01/30/2026 — https://www.varomoney.com/high-yield-savings-account/ ([Varo Bank][1])

- Checking and Savings Promotion and Account Terms — SoFi Bank — 05/28/2026 — https://www.sofi.com/banking/ ([SoFi][2])

- Platinum Savings Account — CIT Bank — 01/09/2026 — https://www.cit.com/cit-bank/platinum-savings ([Citigroup][3])

- High Yield Online Savings Account — Marcus by Goldman Sachs — 05/29/2026 — https://www.marcus.com/us/en/savings/high-yield-savings ([Marcus][4])

- Cash Account — Wealthfront — 01/30/2026 — https://www.wealthfront.com/cash ([Wealthfront][5])

Affiliate Disclosure: AlphaPulse may earn a commission from purchases made through links on this page. Our recommendations are based on independent analysis, and partnerships do not influence our editorial evaluation.