Mortgage rates are climbing back toward 7%, and the math for homebuyers this summer just got tougher. The 30-year fixed averaged 6.51% in Freddie Mac's Primary Mortgage Market Survey for the week ending 05/21/2026, up from 6.36% the prior week. Daily lender surveys are running hotter — Zillow data put the average 30-year purchase rate at 6.627% on 05/27/2026, with refinance rates at 6.733%.

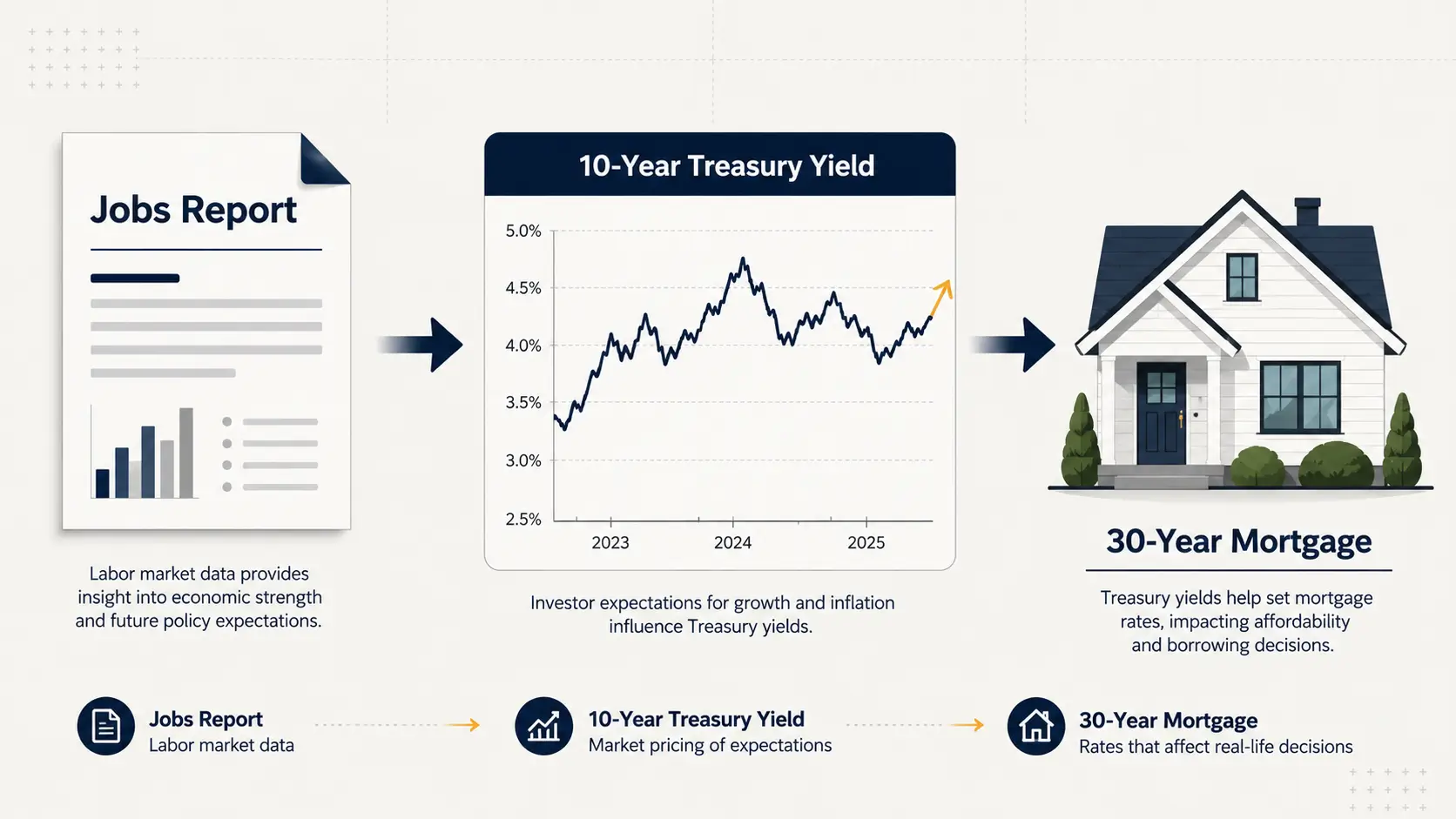

The driver is straightforward and unpleasant. April CPI printed at 3.8% year-over-year on 05/12/2026, the highest annual reading since May 2023. Energy prices, pushed higher by the conflict in Iran, accounted for more than 40% of the monthly increase. Fed funds futures now imply roughly an 80% probability of a rate hike by December 2026 — a full reversal from the rate-cut expectations that prevailed in March. The 10-year Treasury yield, the anchor for mortgage pricing, sits at 4.50% as of 05/27/2026.

Mortgage rates do not track the Fed funds rate directly — they follow the 10-year yield plus a lender spread. That relationship between Treasury yields and mortgage pricing is what determines whether the typical 30-year loan costs 6.5% or 7.25% by the end of summer.

What a Quarter-Point Costs at Three Loan Sizes

For a borrower comparing today's 6.51% Freddie Mac rate to a plausible 7.25% scenario if yields keep grinding higher, the affordability gap widens fast.

On a $300,000 loan, the monthly principal-and-interest payment moves from roughly $1,896 to $2,047 — about $151 more per month, or $54,000 over the life of the loan.

On a $500,000 loan, the payment moves from $3,160 to $3,411 — $251 more per month, or $90,000 over 30 years.

On a $750,000 loan, the payment moves from $4,741 to $5,117 — $376 more per month, or $135,000 over 30 years.

Those figures exclude property taxes, insurance, and PMI, which can add 25% to 40% to total monthly housing costs. As we covered in our analysis of how higher rates are reshaping household budgets, the squeeze compounds when wage growth lags inflation. Real average hourly earnings fell 0.5% in April 2026 and 0.3% over the past 12 months.

Lock or Float — The Decision Frame This Week

The conventional wisdom on rate locks reverses depending on which direction risk is skewed. With markets now pricing rate-hike odds near 80%, the asymmetry has shifted toward locking.

If a buyer is within 30 to 45 days of closing, locking now removes upside risk. The cost of being wrong on a lock if rates fall 0.25 points by closing is usually a few thousand dollars in foregone savings. The cost of being wrong on a float if rates climb 0.25 points is that difference compounded over 30 years of payments.

Float-down options, offered by some lenders for a fee of roughly 0.25% to 0.50% of the loan, let borrowers capture lower rates if they fall before closing. For buyers with closing dates more than 45 days out, the float-down can be worth pricing — but the fee usually pays off only if rates drop by at least 0.50 points.

"As rates fluctuate, aspiring buyers should remember that by shopping around for the best mortgage rate and getting multiple quotes, they can potentially save thousands," Freddie Mac Chief Economist Sam Khater said in the 05/21/2026 PMMS release.

When Refinancing Would Actually Pay Off

For buyers who lock at 6.5% or higher this summer, the refinance math runs through the 10-year yield and the spread above it. The current mortgage-to-Treasury spread is wide — roughly 2.0 percentage points versus a historical norm of 1.7 to 1.8. As that spread normalizes, mortgage rates can fall even if Treasury yields hold steady.

A reasonable refi trigger is a 0.75 to 1.0 percentage-point drop from the original rate, given that closing costs run 2% to 5% of the loan balance. For a borrower locking at 6.75% today, that means a target rate near 5.75% — implying a 10-year yield around 3.75% to 4.00%, depending on spread compression. That level is well below the current 4.50%, but it is the threshold worth watching.

The April PCE inflation report due 05/30/2026 and the next Freddie Mac PMMS release on 05/28/2026 will shape the next two-week direction. If energy retreats and core PCE prints below consensus, the 10-year could give back recent gains and pull mortgage rates back toward 6.3%. If oil holds above $90 and Fed rhetoric stays hawkish, a 7-handle on the 30-year fixed before July remains the path of least resistance.

FAQ

Are mortgage rates expected to drop in summer 2026? Probability has fallen sharply. As of 05/27/2026, Fed funds futures imply roughly 80% odds of a rate hike by December rather than a cut. Mortgage rates can still drift lower if the mortgage-to-Treasury spread normalizes, but a meaningful decline likely requires the 10-year yield to fall below 4.20%.

Should I lock my mortgage rate now or wait? For closings within 30 to 45 days, locking is the lower-risk choice given that rate-hike odds outweigh rate-cut odds. Buyers with later closing dates can ask lenders about float-down options, but the typical 0.25% to 0.50% fee only pays off if rates fall at least 0.50 percentage points.

How much does a 0.75% higher mortgage rate cost over 30 years? On a $300,000 loan, roughly $54,000. On a $500,000 loan, roughly $90,000. On a $750,000 loan, roughly $135,000. These figures cover principal and interest only and exclude taxes, insurance, and PMI.

What 10-year Treasury yield would make refinancing worthwhile? For a borrower at 6.75%, a refinance typically becomes attractive when rates drop at least 0.75 points to around 5.75%. Given a normalized mortgage-Treasury spread, that requires the 10-year yield around 3.75% to 4.00%.

Sources and Further Reading

- Mortgage Rates — Freddie Mac PMMS — 05/21/2026 — https://www.freddiemac.com/pmms

- Today's Mortgage Rates Move Moderately Lower: May 27, 2026 — U.S. News — 05/27/2026 — https://money.usnews.com/loans/mortgages/articles/mortgage-rates-today-may-27-2026

- CPI inflation April 2026: Prices rose 3.8% annually — CNBC — 05/12/2026 — https://www.cnbc.com/2026/05/12/cpi-inflation-april-2026-.html

- US 10 Year Treasury Note Yield Quote and Analysis — Trading Economics — 05/27/2026 — https://tradingeconomics.com/united-states/government-bond-yield